What is the Bitcoin halving?

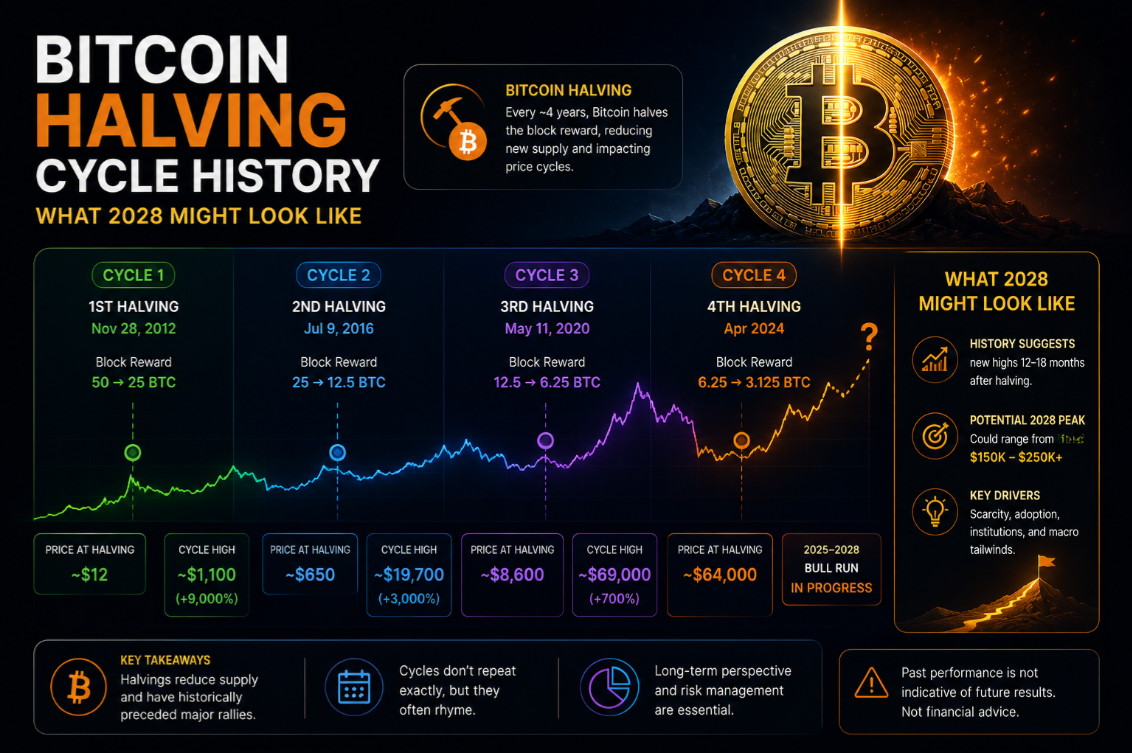

Every 210,000 blocks — roughly four years — the reward paid to Bitcoin miners for validating a block is cut in half. This event, known as the halving (or halvening), is hard-coded into the Bitcoin protocol by Satoshi Nakamoto as the mechanism that enforces Bitcoin's fixed supply of 21 million coins. The last Bitcoin will be mined around 2140.

The halving matters because it directly reduces the rate at which new BTC enters circulation. When demand stays constant or grows while new supply contracts, basic economics predicts upward price pressure. History has validated this prediction three times — though the magnitude and timing of each bull run has differed significantly.

The 2012 halving: from $12 to $1,100

The first halving occurred on 28 November 2012 at block height 210,000. The block reward dropped from 50 BTC to 25 BTC. At the time, Bitcoin was trading at around $12 per coin with a market cap well under $150 million.

Over the following 12 months, Bitcoin surged to a peak of approximately $1,100 in November 2013 — a gain of roughly 9,100% from the halving price. The parabolic run was driven partly by early adopter enthusiasm, the Silk Road narrative, and Cyprus's banking crisis drawing attention to alternatives to traditional finance.

The correction that followed was brutal: Bitcoin fell to around $200 by early 2015, a decline of more than 80% from the peak. This drawdown pattern — rapid parabolic expansion followed by an extended bear market — would repeat in subsequent cycles.

The 2016 halving: institutional seeds and the $20,000 peak

The second halving on 9 July 2016 at block 420,000 cut the reward from 25 BTC to 12.5 BTC. Bitcoin traded at roughly $650 on halving day. The bull run that followed was slower to develop: Bitcoin spent the rest of 2016 consolidating before breaking out in 2017.

By December 2017, Bitcoin reached approximately $20,000 — a 2,970% gain from the halving price. This cycle introduced ICO mania and the first serious wave of retail FOMO. It also attracted the first serious institutional commentary, with CME launching Bitcoin futures in December 2017 just as the peak arrived.

The bear market that followed erased around 84% of the peak price. Bitcoin found a cycle bottom near $3,200 in December 2018 — a pattern later called "crypto winter." The 2016 cycle also confirmed that halving rallies take time: the peak arrived roughly 17 months after the halving event.

The 2020 halving: institutional adoption and $69,000

The third halving occurred on 11 May 2020 at block 630,000. The reward dropped from 12.5 BTC to 6.25 BTC. Bitcoin was trading at around $8,700, having partially recovered from the COVID-19 crash of March 2020 that briefly sent prices to $3,800.

This cycle was different in character. MicroStrategy began accumulating Bitcoin as a treasury reserve asset in August 2020. Square, Tesla, and eventually a string of S&P 500 companies followed. Grayscale Bitcoin Trust saw record inflows. El Salvador adopted Bitcoin as legal tender in September 2021.

Bitcoin peaked at approximately $69,000 in November 2021 — roughly 692% above the halving price, and 18 months after the halving. The subsequent bear market — accelerated by the Terra/LUNA collapse in May 2022 and the FTX implosion in November 2022 — brought Bitcoin down to around $15,500, a drawdown of approximately 78% from the peak.

For the current Bitcoin price and market context, see our Bitcoin market page.

The 2024 halving: ETFs changed everything

The fourth halving occurred on 20 April 2024 at block 840,000, reducing the reward from 6.25 BTC to 3.125 BTC. Unlike previous cycles, this halving arrived with a structural demand catalyst already in place: the SEC approved the first US spot Bitcoin ETFs in January 2024, just three months before the halving.

BlackRock's iShares Bitcoin Trust (IBIT) and Fidelity's Wise Origin Bitcoin Fund alone absorbed tens of billions of dollars in inflows within months of launch. This pre-halving institutional demand helped push Bitcoin to a new all-time high of $73,700 in March 2024 — before the halving even arrived, breaking the historical pattern of post-halving peaks.

The 2024 cycle illustrated how institutional access can pull forward demand that historically built up gradually. For a detailed breakdown of Bitcoin ETF mechanics, see our separate ETF guide on this site.

Comparing cycle returns: diminishing but still substantial

Each halving cycle has produced meaningful gains, with some moderation in percentage terms:

- 2012 cycle: peak gain from halving price approximately +9,100%

- 2016 cycle: peak gain from halving price approximately +2,970%

- 2020 cycle: peak gain from halving price approximately +692%

- 2024 cycle: ongoing; ATH ~$73,700 pre-halving with post-halving trajectory uncertain

The trend of diminishing percentage returns is expected and mathematically consistent with a maturing asset with growing market capitalisation. A move from $8,700 to $69,000 requires significantly less absolute capital than a move from $12 to $1,100 requires in percentage terms.

For a forward-looking view on price targets, our Bitcoin forecast page covers analyst models for the 2024–2028 cycle in detail.

The stock-to-flow model and its limitations

The stock-to-flow (S2F) model, popularised by analyst Plan B in 2019, attempts to quantify Bitcoin's scarcity by comparing existing supply (stock) to annual new issuance (flow). After each halving, the S2F ratio doubles — similar to gold and silver, which have historically commanded premium valuations.

S2F predicted a $100,000+ Bitcoin price in 2021. Bitcoin fell short. Critics argue the model treats Bitcoin as if it were a commodity whose price is purely supply-driven, ignoring demand shocks, regulatory risk, and macro conditions. While S2F has contributed important framing around Bitcoin scarcity, it should not be used as a standalone price prediction tool.

A more robust approach combines S2F scarcity logic with on-chain metrics (MVRV ratio, SOPR, exchange outflows), macro indicators (real yields, dollar index), and adoption signals (ETF flows, corporate treasury announcements).

What could the 2028 halving cycle look like?

The fifth halving is projected for approximately April 2028 at block 1,050,000. The reward will drop from 3.125 BTC to 1.5625 BTC. By that point, over 97% of all Bitcoin will have been mined. Annual new issuance will fall to roughly 164,000 BTC — compared to approximately 900 BTC per day in the 2020–2024 period.

Several structural factors could amplify the 2028 cycle beyond historical norms. Bitcoin ETFs have created a persistent demand pipeline from retirement accounts and wealth management platforms. Nation-state Bitcoin reserves — already established by El Salvador and rumoured at the US federal level — could add sovereign demand. Layer 2 solutions like the Lightning Network and BitVM are expanding Bitcoin's utility as programmable money.

Counterbalancing risks include regulatory tightening in major economies, competition from other digital asset classes, miner revenue stress as block subsidies decline (fee revenue must compensate), and the simple possibility of macro recession dampening risk appetite before the cycle peaks.

For investors considering exposure ahead of the 2028 cycle, our exchange ratings and Coinbase review can help identify platforms suitable for long-term accumulation.

Miner economics and the fee transition

Bitcoin miners currently receive both a block subsidy and transaction fees. As subsidies decline with each halving, the fee component must grow to sustain miner profitability and network security. In the long run, Bitcoin's security model depends entirely on fee revenue.

In 2024, Ordinals inscriptions and BRC-20 token activity temporarily spiked fees to levels not seen since 2017. If Layer 2 activity, Ordinals, and future Bitcoin-native applications generate sustained on-chain fee pressure, the miner revenue problem becomes much less severe. If not, Bitcoin faces a long-term security budget challenge that no halving can solve.

Dollar-cost averaging through the halving cycle

Timing the exact halving peak is notoriously difficult. Most retail investors who tried to sell at cycle tops in 2013, 2017, or 2021 either sold too early or too late. Research on dollar-cost averaging (DCA) shows that regular fixed-amount purchases across both bull and bear phases consistently outperform lump-sum timing attempts for most individuals.

A simple DCA strategy — buying a fixed dollar amount of Bitcoin weekly or monthly regardless of price — removes the emotional burden of timing and benefits from bear market accumulation. Our Bitcoin DCA article on this site models historical return scenarios across different entry points and contribution amounts.

For readers ready to start accumulating, see our Binance review for one of the lowest-fee platforms for recurring Bitcoin purchases.

Key on-chain signals to watch before the 2028 halving

- MVRV Z-Score: values above 7 have historically indicated cycle peaks; values below 0 indicate undervaluation.

- SOPR (Spent Output Profit Ratio): above 1 indicates holders are selling at profit (common near peaks); below 1 indicates capitulation.

- Exchange BTC reserves: sustained outflows from exchanges typically signal long-term accumulation and reduce liquid sell-side supply.

- Miner outflows: large miner transfers to exchanges often precede local tops as miners lock in profits.

- ETF net flows: persistent positive flows from institutional products represent a demand signal without on-chain precedent in earlier cycles.

Key takeaways

Every Bitcoin halving has been followed by a significant price appreciation cycle, though the magnitude has moderated as market capitalisation has grown. The 2024 halving arrived with the structural novelty of US spot ETFs, which pulled institutional demand forward in an unprecedented way. The 2028 halving will occur in an environment where Bitcoin is a recognised asset class, sovereign reserves may exist, and on-chain fees will carry increasing weight in the security model.

History does not repeat exactly, but it rhymes. For investors, the most important lesson from four halving cycles is not when the peak will arrive — it is that the accumulation phase in the years before a halving has historically been the best long-term entry window.

This article is for informational purposes only and does not constitute financial advice. Past halving cycles are not a guarantee of future returns. Cryptocurrency investments carry significant risk.