The centralisation problem in AI

By the end of 2024, four companies controlled the majority of frontier AI capability: OpenAI, Google DeepMind, Anthropic, and Meta. Each runs models trained on hundreds of billions of parameters using tens of thousands of proprietary GPUs. The cost, the data, and the talent required to compete at the frontier are so high that only well-capitalised corporations can play.

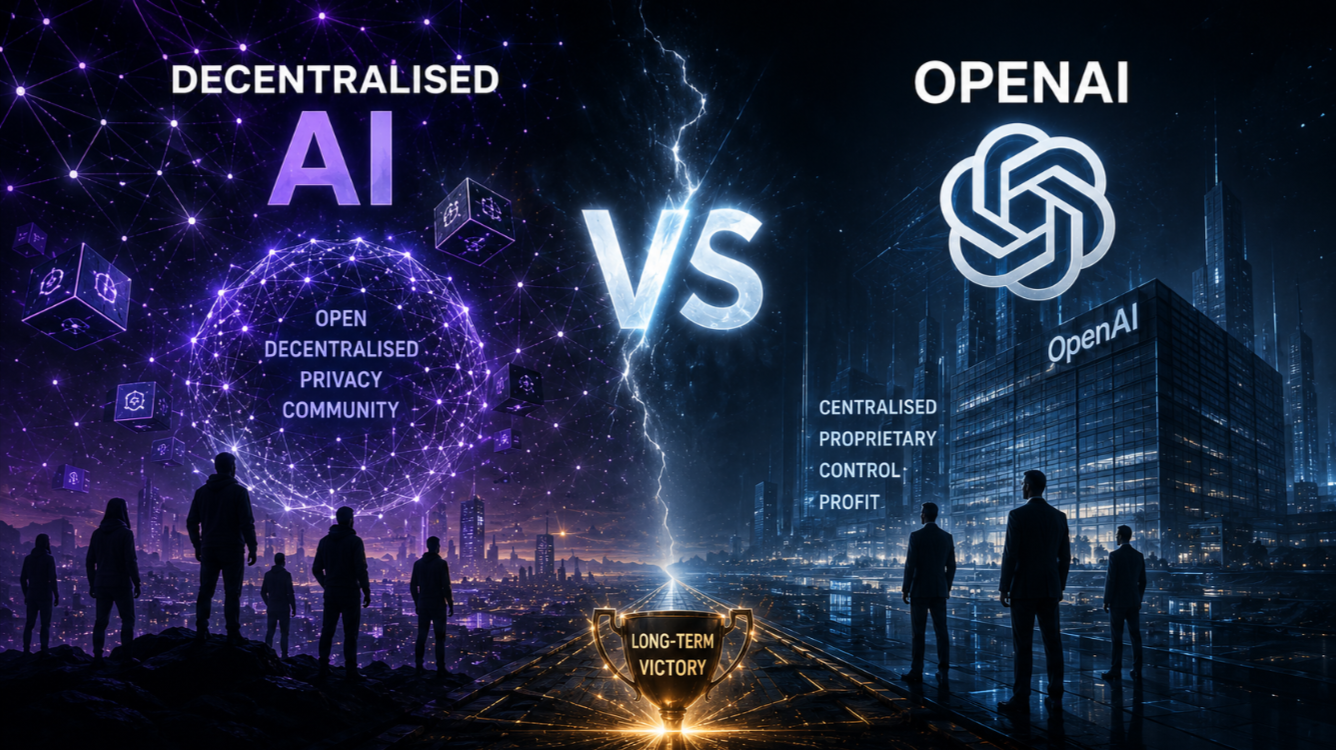

This concentration raises questions that go beyond competitive dynamics. Who decides what a frontier model refuses to say? Who profits from AI-generated economic output? Who is liable when an AI agent makes a costly mistake? Decentralised AI protocols argue that blockchain-based infrastructure offers a fundamentally different answer to all three questions.

What decentralised AI actually means

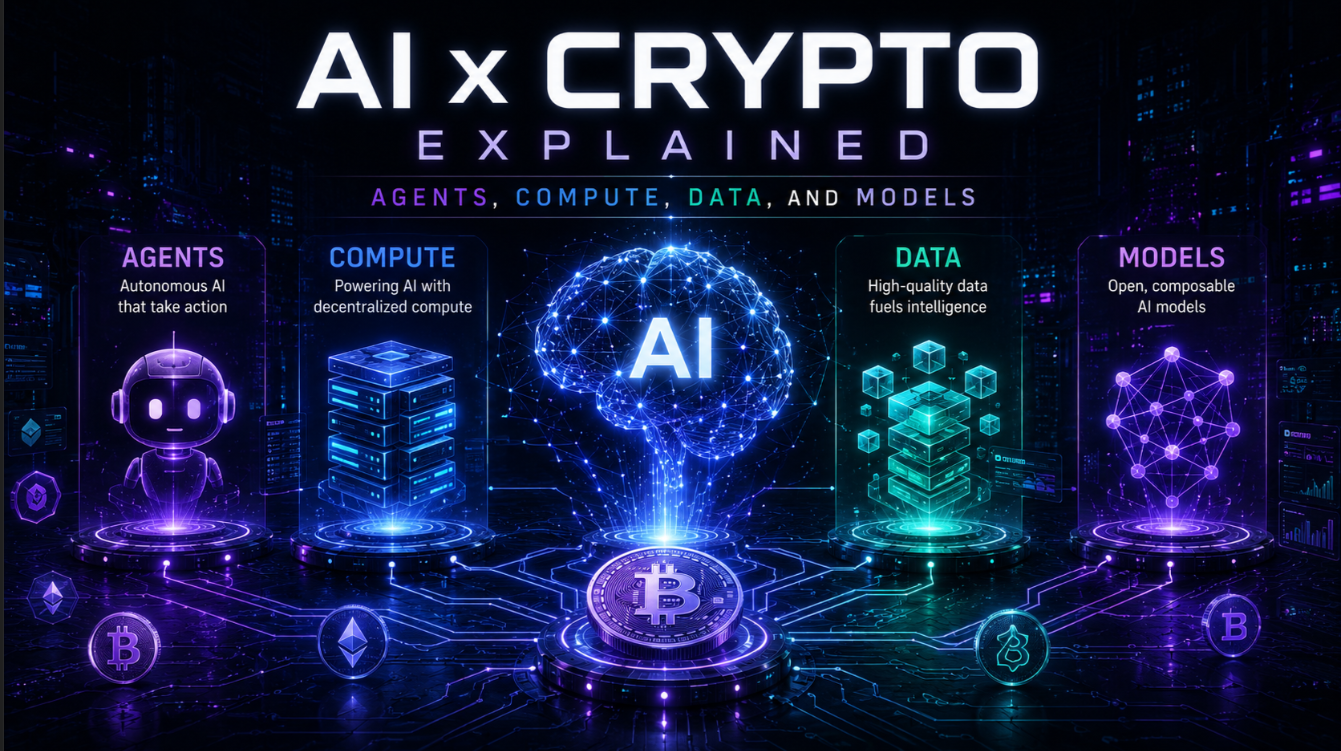

Decentralised AI does not mean running ChatGPT on a blockchain. It means that critical components of the AI stack — compute, data, model weights, inference, agent coordination — are governed and operated by a distributed network rather than a single company.

- Decentralised compute: GPUs contributed by independent operators worldwide rather than owned by one cloud provider.

- Decentralised data: training datasets owned by contributors, with on-chain provenance and automated royalty payment.

- Decentralised models: model weights stored on-chain or in distributed storage, governed by token holders rather than a board of directors.

- Decentralised inference: AI queries routed to the best available model across a network of competing providers rather than a single API endpoint.

Bittensor is currently the most ambitious attempt to build all of this at once through its subnet architecture. You can track the project on the Bittensor market page.

Where centralised AI has decisive advantages today

It is important to be honest about where OpenAI and its peers are currently winning — and why those advantages are hard to overcome quickly.

- Data quality: years of RLHF (reinforcement learning from human feedback) at scale has produced models with nuanced instruction-following. Replicating this with decentralised data labelling is technically feasible but slower.

- Capital: OpenAI raised $6.6 billion in 2024 at a $157 billion valuation. Most decentralised AI projects have treasuries measured in the hundreds of millions at best.

- Brand and distribution: ChatGPT has over 200 million weekly active users. A better technical alternative means nothing if developers and consumers stick with the familiar brand.

- Regulatory relationships: OpenAI, Google, and Microsoft are deeply integrated into government AI advisory bodies. Decentralised protocols have minimal representation in these conversations.

Where decentralised AI has structural advantages

Despite the disadvantages, decentralised AI protocols have structural properties that centralised companies cannot easily replicate.

- Censorship resistance: no single company can be pressured to remove a model or block access for users in certain jurisdictions. This matters for scientific research, journalism, and governance applications.

- Permissionless innovation: anyone can deploy a new subnet, model, or agent protocol without seeking approval from a platform owner. The pace of experimentation in open ecosystems consistently surprises closed ones.

- Economic alignment: token incentives can align the interests of compute providers, data contributors, model developers, and end users in ways that are structurally impossible in a corporation where shareholders come first.

- Long-run cost: aggregating idle compute is structurally cheaper than building and operating purpose-built data centres. As the infrastructure matures, decentralised compute could undercut cloud pricing substantially.

The NEAR Protocol AI thesis

NEAR Protocol has made AI-native blockchain infrastructure its primary strategic focus. The project argues that the next wave of AI agents — software programs that can autonomously transact, negotiate, and operate businesses — needs a blockchain with human-readable accounts, sub-cent fees, and JavaScript accessibility.

The NEAR AI initiative has funded dozens of projects building AI agents on the NEAR stack. If the agent economy grows as projected, NEAR could become the default settlement layer for autonomous AI — a very different competitive position from being just another smart contract platform. Track the ecosystem on the NEAR market page.

The ASI Alliance: merging to compete with OpenAI

In 2024, Fetch.ai, Ocean Protocol, and SingularityNET merged their tokens under the Artificial Superintelligence Alliance (ASI Alliance), with a combined FDV targeting the capital needed to build a credible alternative to frontier centralised AI. The FET token became the unified token of the alliance.

The logic: no single decentralised AI project has the resources to compete with OpenAI alone, but a combined infrastructure stack — Fetch.ai's agent layer, Ocean's data marketplace, and SingularityNET's model marketplace — could address the full stack. The Fetch.ai market page tracks the FET token that represents the alliance.

Open-source AI as a middle ground

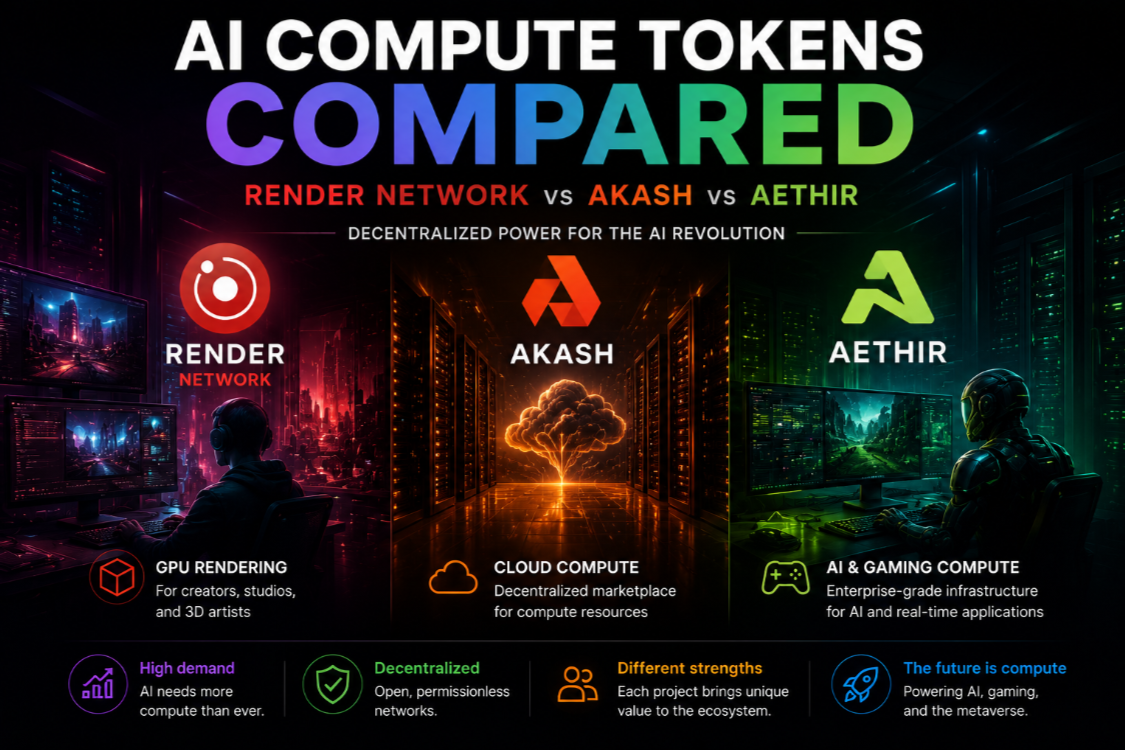

Meta's Llama series, Mistral, and Falcon are open-source AI models that sit between fully centralised (OpenAI) and fully decentralised (Bittensor). They are free to run and modify, but they are still trained and released by centralised entities. Open-source models are already running on decentralised compute networks like Akash and Render, creating a hybrid stack that many developers prefer for its flexibility.

The decentralised AI thesis does not require beating OpenAI at frontier model quality. It only requires building the infrastructure layer that open-source models run on — a more achievable goal, and one that is already happening.

Governance and accountability in decentralised AI

One of the least-discussed but most important aspects of this debate is accountability. When an OpenAI model produces harmful content, there is a company to hold responsible, a board to apply pressure to, a regulatory body to investigate. When a fully decentralised AI system produces harm, accountability is diffuse and enforcement is difficult.

Well-designed decentralised protocols address this with on-chain governance and staking-based accountability. Validators who certify bad outputs lose their staked collateral. But this only works if the governance is genuinely engaged and the penalties are economically meaningful — two conditions that many current protocols do not fully satisfy.

Scenarios for the next five years

- Centralisation wins: OpenAI, Google, and a few others consolidate the AI market. Decentralised protocols remain niche infrastructure, used primarily by developers who want censorship resistance or privacy guarantees.

- Co-existence: centralised AI dominates consumer applications; decentralised AI powers the infrastructure layer — compute, data, agent coordination — with open-source models running on decentralised hardware. This is the most likely scenario.

- Decentralisation wins: a combination of regulatory backlash against AI monopolies, breakthrough efficiency gains in decentralised compute, and a killer agent application drives mainstream adoption of decentralised AI protocols. Long-shot, but not impossible.

What the outcome means for AI token prices

Token prices ultimately reflect expectations about future utility and scarcity. The co-existence scenario — decentralised AI as infrastructure layer — is actually the most bullish for tokens like Render, FET, and TAO, because it gives them large, defensible markets without requiring them to beat OpenAI at consumer products.

The risk is the first scenario: if centralised AI successfully builds proprietary hardware and data moats that make decentralised alternatives uncompetitive on price and quality, the token value proposition weakens significantly. Monitor the compute price gap between centralised cloud and decentralised networks as the most important leading indicator.

This article presents multiple perspectives on the AI centralisation debate. It does not constitute investment or technology advice.