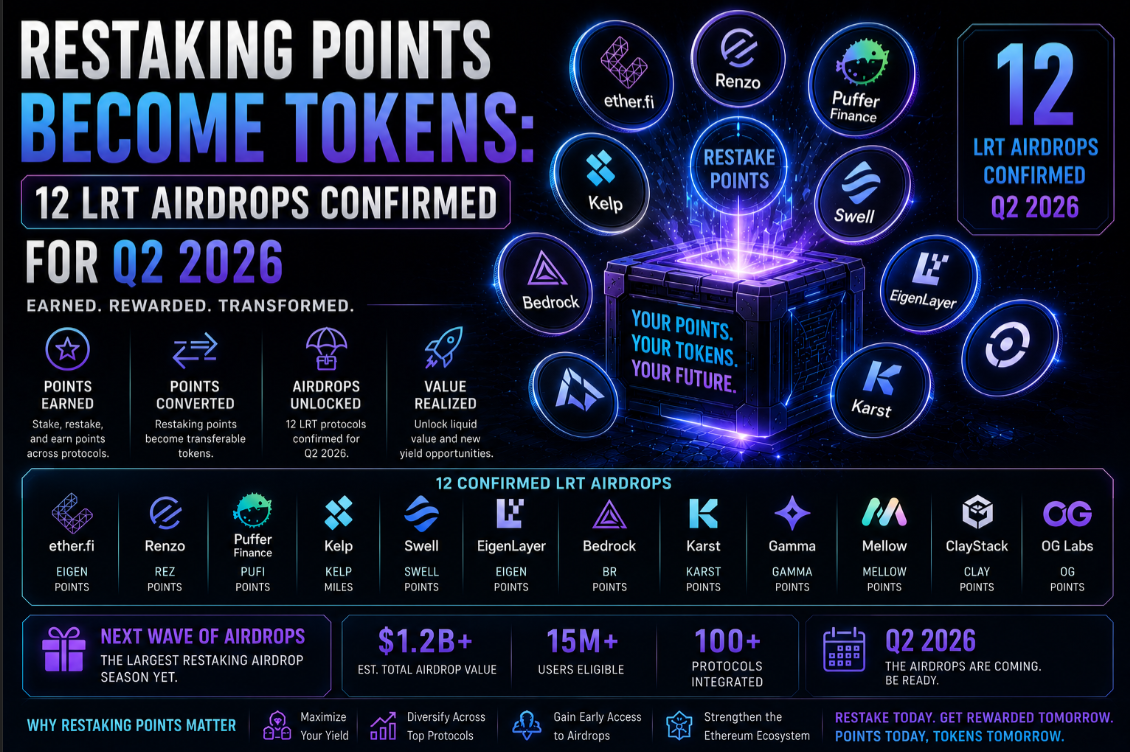

The liquid restaking sector is entering a new phase of maturity in Q2 2026: after 18 months of points programs that rewarded early depositors with opaque off-chain ledger entries, twelve protocols have confirmed they will convert those points to on-chain governance tokens through retroactive airdrops. The announcements represent billions of dollars in new token supply and the settlement of a massive speculative bet made by hundreds of thousands of DeFi participants. Track the underlying EigenLayer ecosystem on the EigenLayer market page.

How We Got Here: The Restaking Points Meta

EigenLayer launched its mainnet restaking in early 2024 with no token and explicit promises that points — denominated in "EigenLayer Points" — would factor into a future distribution. The absence of a token was a deliberate choice: the team wanted to build genuine protocol usage before creating speculative token dynamics. The unintended consequence was a points market: protocols like ether.fi, Renzo, and Puffer wrapped EigenLayer positions into liquid tokens and layered their own points programs on top, creating a recursive reward structure.

Users who deposited early earned EigenLayer Points, LRT protocol points, and — where applicable — DeFi integration points (e.g., Pendle's Points farming multiplier for PT-LRT holders). By Q4 2024, some aggressive depositors had accumulated exposure to four or five simultaneous points programs on the same capital. TVL in liquid restaking protocols peaked at around $18B before the first wave of token distributions partially resolved the accumulated positions.

The Q2 2026 wave represents a second generation of launches — protocols that either delayed their initial distribution or are issuing supplementary governance tokens after observing the first round. For a deep dive into how restaking economics interact with Ethereum's security, see the Lido full review which covers LST/LRT trade-offs, and the staking ratings page for current yield comparisons.

The 12 Confirmed LRT Token Launches

The Q2 2026 cohort of LRT token launches spans both the EigenLayer ecosystem on Ethereum and the Jito Vault/Solana restaking ecosystem:

- Puffer Finance (PUFFER): Season 2 distribution to post-TGE depositors; 8% of supply allocated to retroactive points

- KelpDAO (KEL): Governance token enabling fee revenue sharing with rsETH holders

- Swell Network (SWELL): Covers both liquid staking (swETH) and restaking (rswETH) depositors

- Inception LRT (INETH): Smaller protocol, 100% community-owned via points distribution

- Bedrock (BR): Multi-asset restaking protocol covering ETH, BTC, and SOL depositors

- Nektar Network: EigenLayer AVS points aggregator converting cross-protocol points

- Jito Vault vaults 1–3: Three separate Solana restaking vault tokens launching sequentially

- Fragmetric: Solana native restaking with NCT governance token

- Symbiotic-native protocol A: Name embargoed pending legal review, confirmed via governance forum

- Karak Network (K): Covers Karak's multi-chain restaking vaults

- Byzantine Finance: Aggregator converting multi-protocol EigenLayer vault points

- Solayer (LAYER): Solana endogenous AVS restaking protocol

Token Design Lessons Learned

The early LRT airdrops were heavily criticised for poor design choices: non-transferable periods that trapped claimants in falling markets, cliff-heavy vesting schedules that triggered sell-offs, and Sybil-filtering heuristics that excluded legitimate small depositors. The Q2 2026 cohort has largely internalised these lessons.

Transferability from day one is now the baseline expectation. Protocols that imposed lockups in 2024 watched their token prices decline relative to unlocked competitors as secondary market demand consolidated around freely tradeable tokens.

Fee sharing has emerged as the preferred utility mechanism: instead of governance voting rights over protocol parameters (which most token holders do not actively use), newer tokens grant proportional claims on protocol revenue — restaking fees, AVS reward cuts, and treasury yield. This creates genuine buy pressure beyond speculation.

Sybil filtering now typically uses on-chain activity scoring rather than wallet count alone. Protocols weight points by: total ETH-days deposited, diversity of DeFi interactions, duration of first deposit, and cross-protocol consistency. This rewards genuine long-term participants while reducing the benefit of spinning up hundreds of dust wallets.

Market Impact: Billions in New Supply

Twelve simultaneous token launches over a 90-day window will introduce substantial new supply to the market. Historical data from the first wave of LRT launches shows a consistent pattern: initial price strength in the week surrounding the airdrop announcement, followed by 30-60% corrections as recipients claim and sell, then a recovery period as genuine holders accumulate discounted tokens.

The aggregate fully-diluted value (FDV) of the twelve Q2 cohort protocols, based on pre-launch OTC trades and points market pricing, is estimated at $8–14 billion combined. Circulating supply at launch will be substantially smaller — most protocols are distributing 10-20% of total supply in retroactive airdrops — but the sell pressure on that float will be significant given the number of points farmers who have no strategic reason to hold governance tokens.

DeFi participants considering LRT token positions should review protocol safety records at the staking ratings page and consult custodian options at Coinbase review for compliant access to restaking products.

What Comes After Points: AVS Revenue as Sustainable Yield

The long-term value proposition of restaking does not depend on airdrop speculation. Once AVSs (oracles, bridges, data availability layers, and co-processors secured by EigenLayer and Symbiotic) begin distributing meaningful revenue to restakers, the yield structure becomes self-sustaining. Current AVS yields are small — most EigenLayer AVSs are in testnet or early mainnet and have not activated fee payment mechanisms — but the pipeline is substantial.

Projections from several research teams suggest that if the top 10 EigenLayer AVSs reach production scale by end of 2026, they could distribute $200-400M annually to restakers. At current EigenLayer TVL, that implies an additional 1.5-3% APR on top of base Ethereum staking yield — a compelling proposition that would rationalise LRT positions on fundamentals rather than points speculation. The EigenLayer market page tracks AVS onboarding progress in real time.