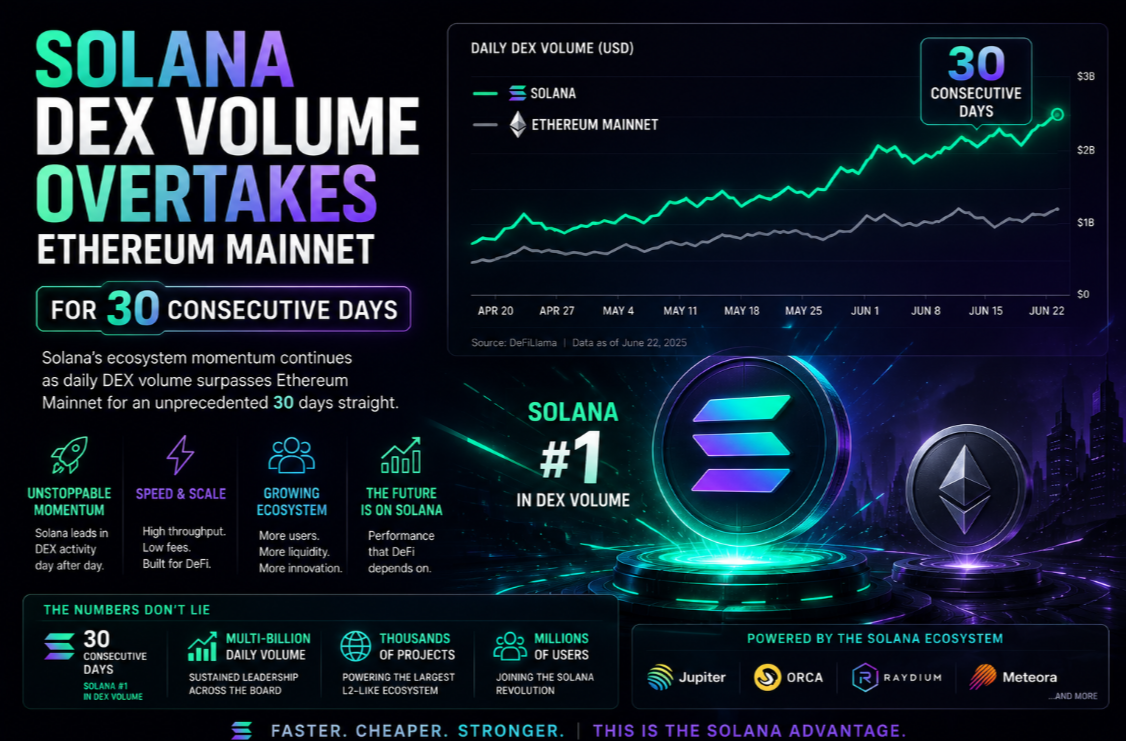

For thirty consecutive days ending April 27, 2026, Solana's decentralised exchanges recorded higher aggregate trading volume than Ethereum mainnet DEXes — a milestone that would have seemed implausible three years ago. The streak marks the first time any blockchain has consistently outtraded Ethereum's native DEX layer and rewrites the competitive landscape for on-chain trading infrastructure.

The Numbers: Solana vs Ethereum Mainnet DEX Volume

Data aggregated from DefiLlama and on-chain analytics shows that Solana's DEX volume averaged $4.2 billion per day over the 30-day period, versus Ethereum mainnet's $3.1 billion. The gap peaked at 2.1× on April 14 — the same day Pump.fun's Raydium migration triggered record fees — before settling to a more typical 1.3–1.5× differential.

- Solana 30-day average: $4.2B/day (April 2026)

- Ethereum mainnet 30-day average: $3.1B/day

- Solana peak single day: $18.7B (April 14)

- Ethereum peak single day: $9.2B (same period)

- Solana DEX dominance over Ethereum: 30 consecutive days

It is important to note that this comparison excludes Ethereum Layer 2 networks. If Arbitrum, Base, Optimism, and other L2 DEX volume is added, Ethereum's broader ecosystem still outvolumes Solana by approximately 1.8×. But the distinction matters: Ethereum mainnet is where the deepest liquidity, largest institutional trades, and most collateralised positions have historically lived.

Jupiter's Role as Aggregation Engine

Jupiter Exchange is the primary reason Solana can claim deep market liquidity despite having fewer total protocols than Ethereum. Jupiter aggregates liquidity across Raydium, Orca, Meteora, Lifinity, and 12 other Solana AMMs into a single routing layer. Users get near-optimal execution on any token pair without manually selecting pools — a UX that matches or exceeds what Uniswap v4's hooks architecture offers on Ethereum.

Jupiter's volume share of total Solana DEX volume has grown from 61% in Q4 2025 to 74% in Q1 2026. This concentration reflects the aggregator's superior routing algorithm rather than a lack of competition — it means more trades are finding optimal execution, which attracts more volume in a positive feedback loop. Jupiter's limit order feature now handles $340M in daily orders, with a fill rate of 91% within the user's price tolerance.

Raydium's CPMM Innovation and Concentrated Liquidity

Raydium's upgrade to CPMM (constant product market maker) pools with concentrated liquidity ranges has dramatically improved capital efficiency for LPs. A liquidity provider can now concentrate their capital in a $120–180 SOL/USDC range, earning 8–12× more fees per dollar deployed than a full-range position. This mirrors Uniswap v3's concentrated liquidity model but is native to Raydium's higher-throughput environment.

The result: Raydium's Total Value Locked (TVL) has grown 240% year-over-year to $3.4 billion, while fee yield for active LPs has averaged 48% APR in meme-coin pools and 12–18% APR in major pair pools. Institutional market-makers who previously operated exclusively on Ethereum CEX/DEX hybrid strategies are increasingly allocating LP capital to Raydium.

Institutional Market-Makers: The Decisive Shift

The volume story would not be credible without institutional depth. In Q1 2026, three of the top five on-chain market-makers by volume (Wintermute, Amber Group, and Flow Traders' on-chain desk) expanded Solana operations to match or exceed their Ethereum DEX exposure. Their reasoning:

- Transaction finality: Solana's 400ms vs Ethereum's 12s block time reduces inventory risk for market-makers

- Fee predictability: Solana's fee model is more predictable than Ethereum's EIP-1559 spikes during congestion

- Cross-protocol composability: A single Solana transaction can route through Jupiter, deposit to Kamino, and borrow against collateral — in one atomic operation

- Lower slippage on mid-cap tokens: Concentrated Raydium pools have narrower spreads than Uniswap v3 equivalent pools for the same TVL

What This Means for SOL Token Economics

Higher DEX volume has a direct tokenomic effect: more swaps mean more Solana transaction fees, which are partially distributed to validators and increase staking incentives. Sustained high volume at current levels would put Solana on track for $800M–$1.1B in annualised on-chain protocol revenue — a figure that justifies a re-rating of SOL's price-to-earnings multiple relative to other L1 platforms.

There is also a liquidity network effect: as more volume flows through Solana, more token projects choose to launch here rather than Ethereum, which brings more users and more volume. The cycle is self-reinforcing — which is precisely why the 30-day streak matters beyond the headline number.

Risks to Solana's DEX Volume Lead

Ethereum L2 competition is the primary risk. Uniswap v4 on Base and Arbitrum One offers competitive fees, Ethereum security guarantees, and the deepest stablecoin liquidity in DeFi. If Base's volume (already at $1.8B/day) migrates more institutional pairs to L2, the Ethereum ecosystem could reclaim mainnet + L2 superiority.

Solana's second risk is protocol concentration: if Pump.fun meme-coin activity cools sharply, a significant chunk of volume disappears. Sustained institutional volume in stablecoin pairs, BTC synthetics, and real-world asset trading would create a more durable foundation. That diversification is underway — non-meme volume grew from 38% to 52% of Solana DEX volume between Q4 2025 and Q1 2026 — but is not complete.

For users looking to participate in Solana's DEX ecosystem, managing assets through a secure wallet is essential. See the full Phantom wallet review for an in-depth look at the primary interface most Solana traders use to access Jupiter and Raydium.