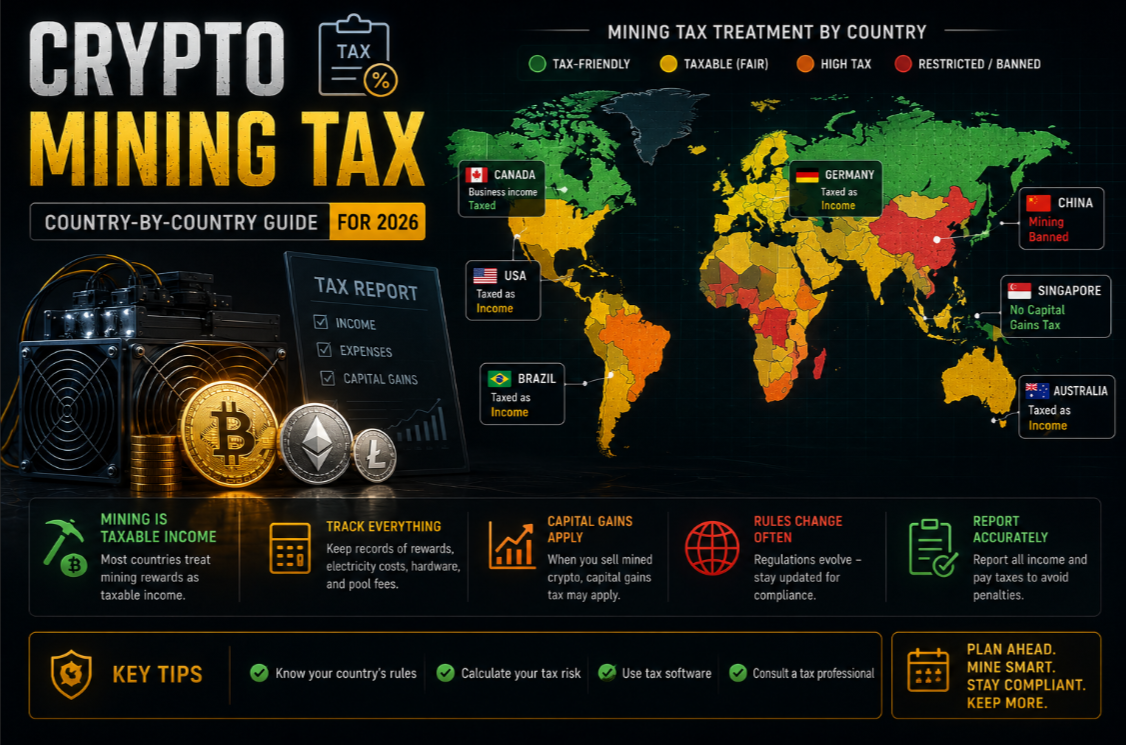

Why mining taxation is complex

Cryptocurrency mining occupies an unusual space in tax law: it simultaneously resembles self-employment income (you perform work and receive compensation), capital asset acquisition (you receive property that will later be sold), and sometimes business income (if conducted at commercial scale). Different tax authorities classify it differently, and the rules have been evolving rapidly as regulators develop specific guidance.

Understanding your tax obligations before you start mining is not optional — it is essential. In most jurisdictions, mined crypto is taxable from the moment you receive it, regardless of whether you sell it. Failing to report mining income is tax evasion, not a grey area. This guide covers the rules in eight major jurisdictions as of 2026.

United States: mining income and self-employment tax

In the United States, the IRS treats mined cryptocurrency as ordinary income at the fair market value on the date received. This applies whether you mine solo or through a pool — each pool payout is a taxable income event.

- Individual (hobby) miners: Report mining income on Schedule 1 as "Other income." Hobby loss rules apply — you cannot deduct expenses beyond income from the activity. No self-employment tax.

- Business miners: If mining is conducted with profit intent and some regularity, it is business income on Schedule C. You can deduct electricity, hardware depreciation, internet, and home office. Self-employment tax (15.3%) applies to net profit.

- Capital gains: When you sell mined BTC, you owe capital gains tax on appreciation since the mining date. Short-term (held <1 year): taxed as ordinary income. Long-term (held >1 year): 0%, 15%, or 20% depending on income bracket.

- Form 1099 reporting: Mining pools above certain thresholds may issue 1099-MISC. Regardless, all mining income is reportable whether or not you receive a form.

Hardware purchases are deductible as business expenses. Under Section 179, you may be able to deduct the full cost in the year of purchase rather than depreciating over several years. Consult a CPA with crypto experience for specifics.

United Kingdom: mining as miscellaneous income or trading

HMRC (Her Majesty's Revenue and Customs) distinguishes between mining as a hobby and mining as a trade, with meaningfully different tax treatment:

- Hobby mining: Income is "miscellaneous income" and must be reported on a Self Assessment tax return. The coins' GBP value at receipt is the taxable amount. Minimal expenses are deductible under hobby rules.

- Trade/business mining: If mining constitutes a commercial activity (regularity, scale, profit motive), it is trading income. You can deduct allowable business expenses including electricity, hardware (capital allowances), and running costs.

- Capital Gains Tax (CGT): When mined coins are sold, CGT applies on gain from mining value to sale value. Annual CGT allowance (£3,000 in 2026) can offset gains. Rate: 18% (basic rate taxpayer) or 24% (higher rate) on crypto gains.

- VAT: Mining itself is not subject to VAT per current HMRC guidance. However, if you sell mining services to third parties, VAT may apply.

Germany: tax-free after one year

Germany has one of the most crypto-friendly tax regimes for long-term holders. The Bundesministerium der Finanzen (BMF) classifies mined cryptocurrency as "other income" (sonstige Einkünfte) under §22 No. 3 EStG at the time of mining.

- Income at mining: The EUR value of coins at the time of mining is taxable as other income. Your marginal income tax rate applies (up to 45% + Solidaritätszuschlag).

- One-year holding privilege: If you hold mined coins for more than one year before selling, the sale is completely tax-free. This is the same treatment as other crypto held long-term under German law.

- Business mining: If mining is conducted as a Gewerbebetrieb (commercial business), different rules apply — Gewerbesteuer (trade tax) on profits, and no tax-free holding period benefit.

- Mining expenses: Electricity, hardware depreciation, and related costs can be deducted against mining income if you operate as a business.

The tax-free sale after one year is a significant advantage for German miners with a long-term holding strategy. Mine, hold for 12+ months, sell tax-free. This is one reason Germany has an active retail crypto mining community.

Australia: income tax and CGT interaction

The ATO (Australian Tax Office) treats mined crypto as assessable income at the AUD market value on receipt, whether the taxpayer is an individual hobbyist or a business.

- Individuals: Mined coins are "ordinary income" and added to total assessable income. Taxed at marginal rate (up to 45%).

- Business: Mining income is business income. Expenses (electricity, hardware, internet) are deductible. GST registration required if annual turnover exceeds $75,000.

- CGT discount: Australia offers a 50% CGT discount on assets held >12 months. If you mine 1 BTC worth $100k AUD, hold it for 13 months, then sell for $150k, you owe CGT on 50% of the $50k gain ($25k × your marginal rate).

- Personal use asset exemption: Does not apply to mined coins acquired primarily for investment.

Canada: business income and CRA guidance

The Canada Revenue Agency (CRA) treats cryptocurrency mining as either business income or a personal pursuit depending on facts and circumstances. Scale, intent, and infrastructure investment are key factors.

- Business mining: Mined coins are business income at FMV on receipt. Expenses fully deductible. 50% of capital gains on disposition are included in taxable income (effective CGT rate = 50% × marginal rate).

- Personal mining: Treated as a barter transaction income. More limited expense deductions. The CRA has been increasingly willing to classify regular mining as business activity.

- GST/HST: Mining services sold to others may be subject to GST/HST. Mining for yourself is generally outside the GST/HST net.

- Foreign reporting: If you hold crypto on foreign exchanges above CAD $100,000, Form T1135 (Foreign Income Verification) may be required.

Netherlands, Portugal, and UAE: three contrasting approaches

Tax treatment varies dramatically across even EU member states:

Netherlands:

Dutch tax law does not tax mining income as realised income. Instead, crypto holdings are included in "Box 3" wealth tax — you pay a flat rate (approximately 1.7% in 2026) on the notional yield from your total wealth above a threshold (€57,000 per person). This means miners are not taxed on mined coins when received, but on the value they hold. Professional mining as a business falls under Box 1 (income tax).

Portugal:

Portugal, once the "crypto tax haven" of Europe, introduced crypto income taxes in 2023. Mining income is now taxable at 28% flat rate (or at personal income tax rates if mining is a professional activity). Coins held more than 365 days before sale remain tax-exempt under a holding period exemption.

United Arab Emirates (UAE):

The UAE has no personal income tax and no capital gains tax for individuals. Mining income received by individuals is therefore tax-free. Businesses operating mining farms in the UAE may fall under the 9% corporate tax introduced in 2023 on profits above AED 375,000. The UAE has become a significant hub for crypto mining operations partly due to this favourable tax treatment.

Record-keeping requirements for miners

Regardless of jurisdiction, comprehensive records are essential:

- Log every pool payout: date, amount in crypto, and USD/local currency equivalent at time of receipt

- Keep records of all hardware purchases (date, cost, seller) for depreciation calculations

- Track electricity costs attributable to mining (dedicated meter or proportional allocation)

- Record all coin disposals: date sold, sale price, original mining value (cost basis)

- Retain all records for at least 5–7 years depending on your jurisdiction's statute of limitations

Crypto tax software such as Koinly, CoinTracker, or CryptoTaxCalculator can automate much of this if you connect your pool accounts and wallets. Manual spreadsheets are also acceptable but error-prone for active miners.

Mining as a business vs hobby: how regulators decide

Most tax authorities use similar factors to determine whether mining is a business or hobby:

- Scale of operation: Multiple machines, dedicated space, and significant capital investment suggest business.

- Profit intent: Do you conduct the activity with an expectation of profit? Have you ever been profitable?

- Time commitment: Do you spend significant time managing the operation, optimising settings, or researching hardware?

- Expertise: Do you have technical knowledge of mining? Have you sought to improve profitability?

- History of income or losses: Consistent losses over multiple years weigh against business classification.

Business classification is generally advantageous (full expense deductibility) but comes with additional compliance obligations (business registration, quarterly taxes, GST/VAT registration thresholds). The decision has significant financial implications — consult a tax professional before claiming business status.

This article provides general information only and does not constitute tax advice. Tax laws change frequently. Consult a qualified tax professional in your jurisdiction for personalised advice on your mining activities.