What is NFT-Fi and why it emerged

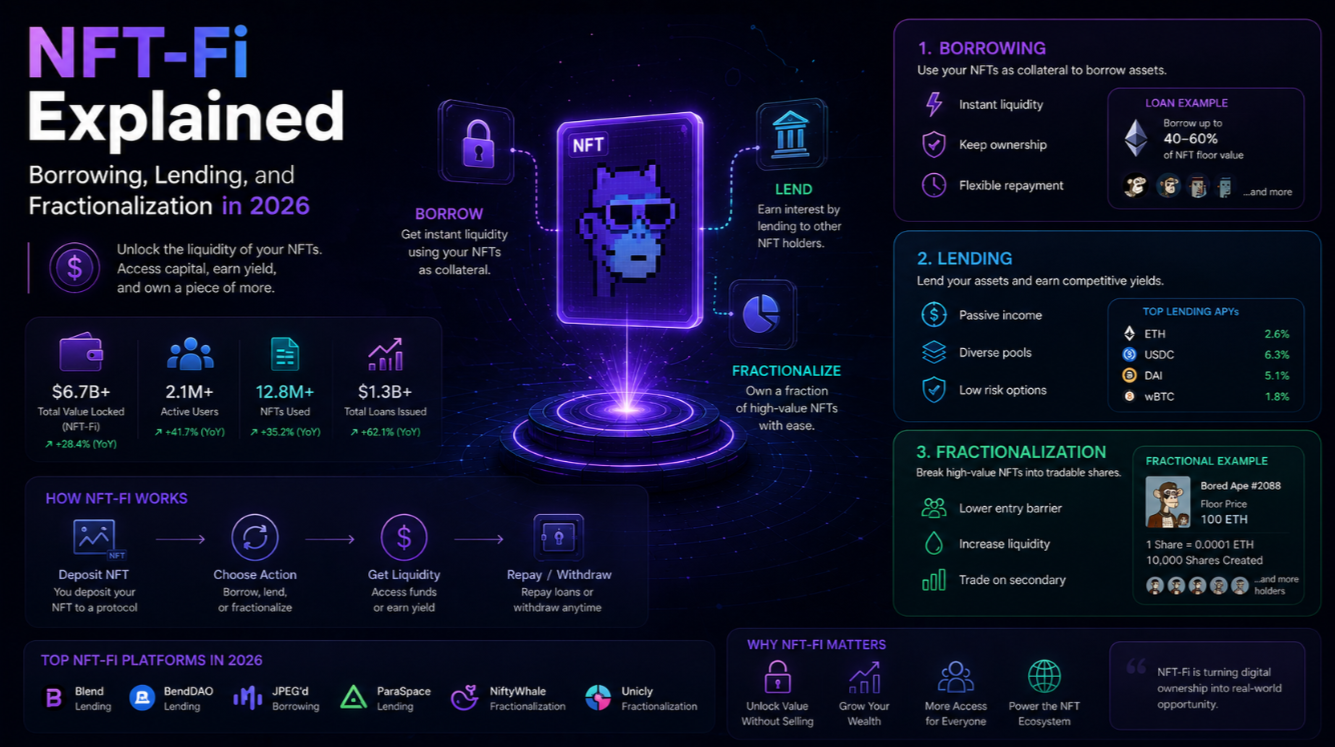

NFT-Fi (NFT Finance) is the umbrella term for DeFi protocols that treat NFTs as financial instruments rather than just collectibles. The core insight is that a blue-chip NFT is an asset — it has a market price, it can serve as collateral, it can be fractionalised into fungible shares, and it can generate yield. NFT-Fi protocols unlock this financial potential.

The motivation is liquidity. NFTs are illiquid by nature — selling a high-value NFT requires finding a buyer willing to pay your price, which can take days or weeks. NFT-Fi protocols let holders access liquidity without selling their asset, similar to a mortgage or pawnshop loan backed by a house or luxury item.

NFT-backed loans: how peer-to-peer lending works

The most developed NFT-Fi category is collateralised lending. The two dominant models are peer-to-peer (P2P) and peer-to-pool (P2Pool).

In P2P lending (pioneered by NFTfi and Arcade), a borrower lists their NFT as collateral and specifies desired loan terms: amount, duration, and interest rate. Lenders browse listings and offer competing loan terms. If the borrower accepts, the NFT is locked in an escrow contract and the borrower receives the loan in ETH or WETH. If the borrower repays principal plus interest by the deadline, they get the NFT back. If they default, the lender keeps the NFT.

Peer-to-pool NFT lending: Blur Blend and BendDAO

P2Pool lending uses an automated mechanism rather than individual lender matching. BendDAO allows users to borrow ETH against blue-chip NFT collateral (BAYC, CryptoPunks, Azuki) up to a loan-to-value (LTV) ratio of around 30–40% of the NFT's floor price. The pool automatically sets interest rates based on utilisation.

Blur NFT's lending product, Blend, introduced a novel perpetual loan model: loans have no fixed duration and only expire when a lender calls the loan (triggering a refinance auction) or the borrower defaults. This reduces the risk of forced liquidation at inopportune times. Blend handled billions in loan volume within weeks of launch.

Key risks of NFT-backed loans

- Liquidation risk: If your NFT's floor price drops sharply, you may be liquidated — the lender seizes the NFT at a value higher than its market price. During market crashes, liquidations can cascade and flood the market, further depressing floors.

- Duration risk: Short-duration loans expire before you can repay if market conditions change. Perpetual models (Blend) reduce this but introduce call risk.

- Smart contract risk: NFT-Fi protocols are complex and have been exploited. BendDAO experienced a near-liquidity crisis in August 2022 when BAYC floors dropped and lenders could not exit.

- Oracle risk: LTV calculations depend on floor price oracles. Manipulating the floor price via wash trading can allow attackers to extract over-collateralised loans.

NFT fractionalization: owning a slice of a blue chip

Fractionalization protocols let the owner of a single high-value NFT split it into thousands of fungible ERC-20 tokens, each representing fractional ownership. The original NFT is locked in a vault contract. Fractional shares can be bought and sold on Uniswap, giving collectors with limited capital access to blue-chip NFTs.

Fractional.art (now Tessera) and Unic.ly pioneered this model. Key mechanics: the vault owner sets an initial share price, shares are distributed via an auction or direct sale, and any shareholder can initiate a buyout auction to acquire the full NFT by bidding above a reserve price. If the buyout succeeds, all shareholders receive their proportional payout in ETH.

The SEC and fractional NFTs: regulatory risk

The SEC has signalled that fractional NFTs may qualify as securities under the Howey test — particularly when they represent investment contracts in a common enterprise with expectation of profit. Several fractionalisation protocols reduced or paused operations after regulatory warnings. Any fractional NFT product in 2026 carries meaningful legal uncertainty, especially for US persons.

NFT rental markets

Rental protocols allow NFT holders to earn yield by temporarily lending their NFT to other users. This is most common in blockchain gaming — a guild or player rents a high-tier game asset they cannot afford to buy. ERC-4907, a rental extension to ERC-721, adds a separate "user" role to an NFT that can be assigned without transferring ownership. When the rental expires, the user role automatically reverts.

ReNFT and Double Protocol are the main rental marketplaces. Yield from gaming NFT rentals was substantial in 2021–2022 but contracted sharply as play-to-earn economics collapsed. Rentals are recovering in 2026 as better-designed games integrate NFT assets with genuine gameplay utility.

NFT yield vaults: put your collection to work

Yield vaults aggregate NFTs from multiple holders, deploy them in NFT-Fi strategies (lending, renting, liquidity provision for collection derivatives), and distribute returns to depositors. Protocols like NFTX create liquidity pools where users can deposit NFTs from a collection and receive ERC-20 vault tokens — which can then be staked for yield or used as collateral.

ApeCoin staking — which allows BAYC, MAYC, and BAKC NFT holders to stake their ApeCoin allocation to earn additional yield — is one of the largest NFT-Fi pools by TVL. Separate NFT staking mechanics tie financial returns directly to NFT ownership, creating a yield layer on top of speculative value.

NFT derivatives and index products

NFT perpetual futures allow traders to speculate on NFT collection floor prices without owning the underlying assets. NFTPerp and Tribe3 offered perpetual contracts on major collections including BAYC, Azuki, and Milady. These products introduce sophisticated DeFi risk dynamics (funding rates, liquidations) into the NFT market.

NFT indices — baskets of blue-chip collections weighted by floor price or liquidity — provide diversified exposure. Metastreet and similar protocols offer structured products with senior and junior tranches of NFT loan pools, adapting TradFi securitisation to digital assets.

How to access NFT-Fi safely

- Start with P2P lending on well-audited platforms: NFTfi and Arcade are the most established, with multi-year track records and multiple audits.

- Use only blue-chip collateral: Illiquid or low-liquidity NFTs are poor collateral — liquidation into a thin market locks in losses.

- Borrow conservatively: Keep LTV below 40% to buffer against floor price volatility. Never borrow more than you can repay from external funds if the NFT value drops.

- Read the liquidation mechanics: Understand exactly at what price and under what conditions your NFT can be seized. Threshold varies significantly by protocol.

The NFT-Fi stack in 2026

NFT-Fi has matured significantly since 2021. Loans, fractionalization, rentals, derivatives, and index products all exist with real TVL and usage. The market is still small compared to DeFi overall, and liquidity is thin relative to the asset values involved. But the infrastructure for treating NFTs as productive financial assets is now in place. The NFT Marketplaces ratings includes NFT-Fi protocol coverage for projects that have integrated financial tooling.

NFT-Fi and the Blur ecosystem

Blur has become more than a trading marketplace — through Blend and its aggregator, it operates as a full NFT-Fi hub. The Blur NFT token reflects platform governance and fee-sharing mechanics that depend on NFT-Fi activity volumes. Understanding the token economics helps evaluate the sustainability of Blur's platform incentives.

NFT-Fi protocols carry compounded risks: smart contract vulnerabilities, NFT price volatility, oracle manipulation, and regulatory exposure. Only deploy capital you can afford to lose entirely.