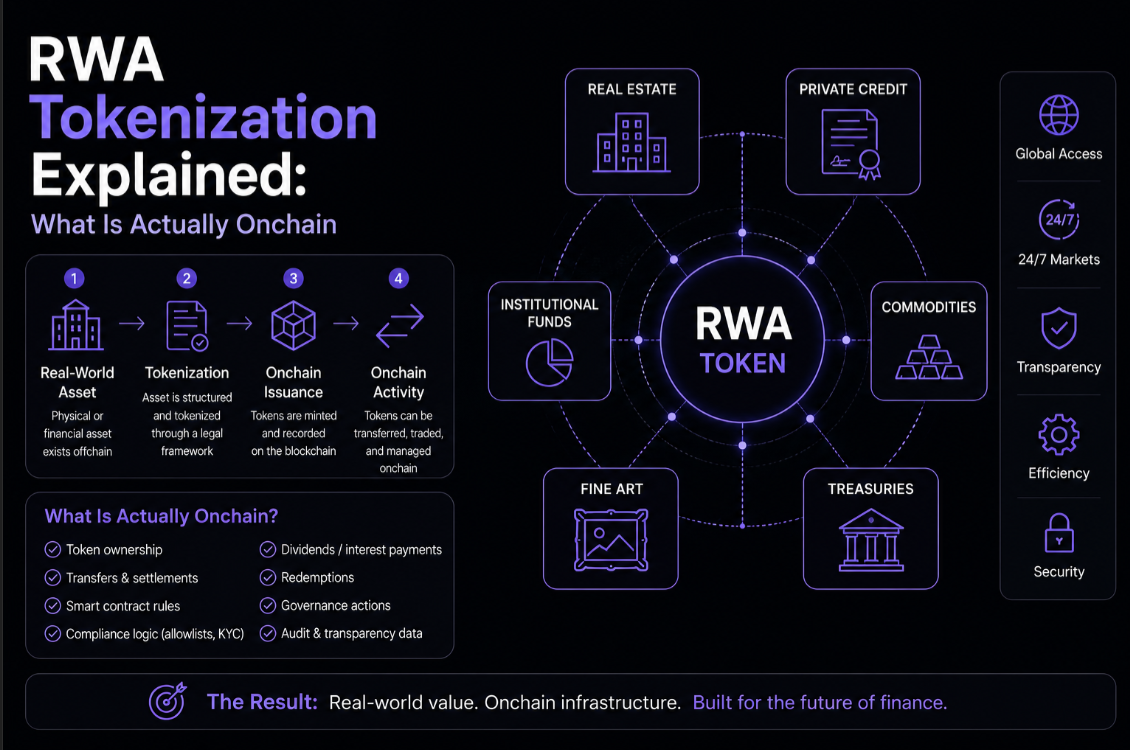

What does "tokenizing a real-world asset" actually mean

Real-world asset (RWA) tokenization is the process of representing a claim on an off-chain asset — a US Treasury bill, a share of a commercial property, a corporate bond, a piece of fine art — as a token on a public or permissioned blockchain. The token acts as a digital certificate: it encodes ownership rights, transfer restrictions, and economic entitlements in programmable code rather than paper contracts held in a custodian vault.

The key word is "claim." When you buy a tokenized Treasury bill, you do not hold the T-bill directly onchain. You hold a token issued by a regulated entity (the issuer) that holds the underlying T-bill in a bankruptcy-remote legal structure. Onchain you have a token; offchain an audited custodian holds the real asset backing it. The blockchain provides settlement finality, programmable compliance, and 24/7 transferability — it does not magically move a physical bond certificate onto Ethereum.

The four layers of a tokenized asset

Every RWA product involves four distinct layers, and understanding them prevents costly mistakes.

- Legal wrapper: A special-purpose vehicle (SPV), trust, or fund structure holds the underlying asset and issues shares or notes to investors. This wrapper defines your legal recourse if the issuer fails.

- Custody: A regulated custodian — a bank, broker-dealer, or licensed trust company — holds the actual asset (e.g., T-bills at a Federal Reserve Primary Dealer, or property title in a land registry). Custody is the off-chain anchor.

- Oracle/attestation: A mechanism that bridges the off-chain asset value to the on-chain token. This can be a third-party audit, a real-time price feed, or a monthly NAV report. Stale or manipulated attestations are a primary risk vector.

- Token contract: The on-chain smart contract that manages token supply, transfer rules (whitelist/KYC checks, lock-up periods), distributions (yield payments), and redemption logic.

Weaknesses in any of these layers create risk. A sound token contract means nothing if the custodian is insolvent or the legal wrapper does not clearly entitle the token holder to the underlying asset.

What is actually onchain vs what stays offchain

A common misconception is that tokenization puts the asset itself onchain. It does not. Here is what each side actually contains:

- Onchain: Token balances, transfer history, yield accrual and distribution logic, KYC/whitelist status, lock-up enforcement, redemption requests.

- Offchain: The underlying asset (bonds, real estate, shares), legal ownership records, regulatory filings, custody agreements, auditor reports, and bankruptcy-remote SPV governance.

The practical result is that the blockchain replaces the transfer agent and settlement layer — the part of the system that tracks who owns what — while traditional legal and custodial infrastructure continues to enforce and protect real ownership. This hybrid model is less radical than crypto-native advocates sometimes claim, but it is also less fragile than fully on-chain experiments with no real-world grounding.

Major asset classes being tokenized in 2026

The RWA tokenization market has grown past $20 billion in on-chain value in 2026. The dominant categories are:

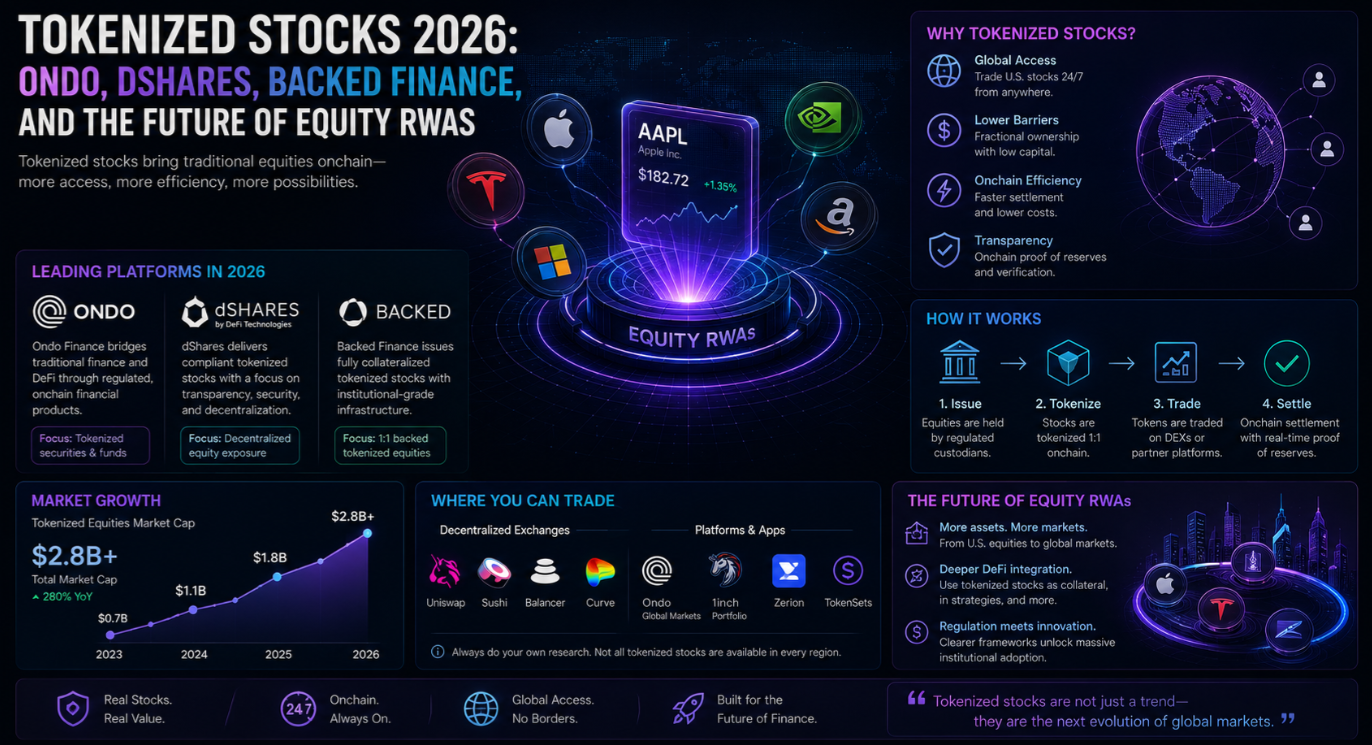

- Tokenized US Treasuries: The fastest-growing segment. Products like BlackRock's BUIDL, Franklin Templeton's FOBXX, Ondo Finance's OUSG and USDY, and Mountain Protocol's USDM collectively hold over $8 billion in on-chain T-bill exposure. Yields of 4–5% in a DeFi-native wrapper drove rapid adoption from stablecoin holders seeking yield.

- Private credit: On-chain loan origination and securitisation through platforms like Maple Finance and Centrifuge. These tokenize business loans, invoice finance, and trade finance into pools that DeFi liquidity providers can fund.

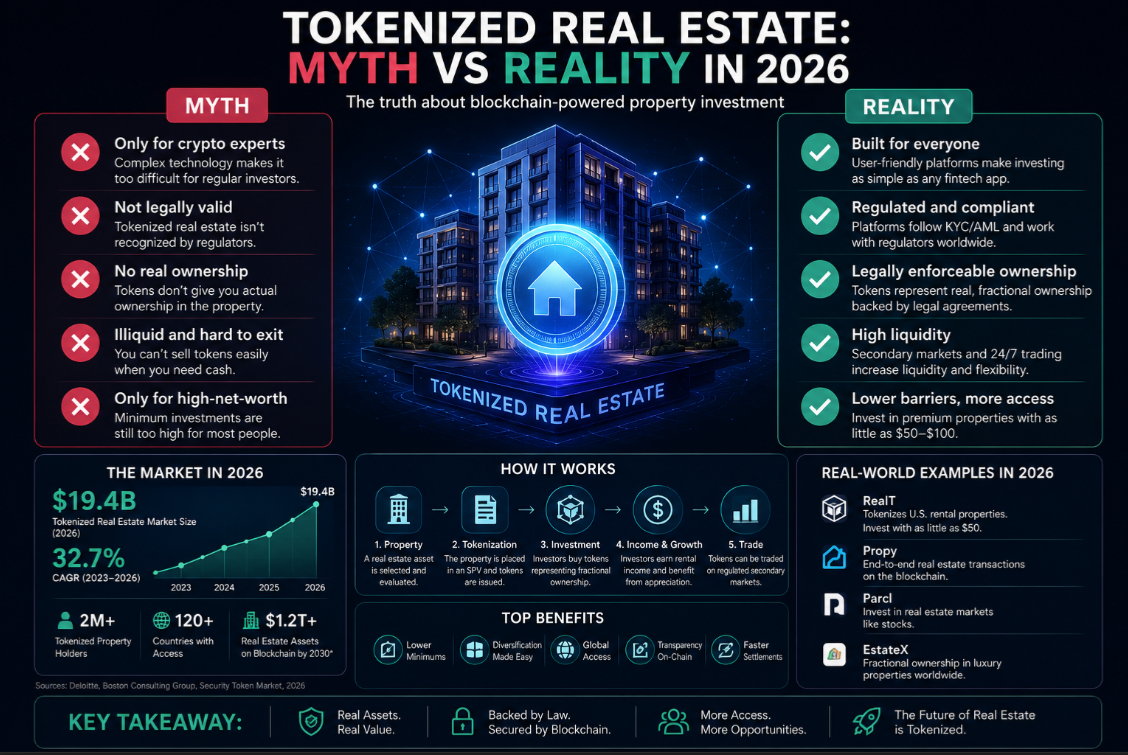

- Real estate: Fractional ownership tokens for individual properties or property funds. Smaller market than Treasuries, with significant regulatory fragmentation by jurisdiction.

- Equities and funds: Tokenized representations of public stocks and ETFs (Backed Finance, Ondo Finance's Ondo Global Markets) and private fund interests.

- Commodities: Gold tokens (Paxos PAX Gold, Tether Gold), oil futures receipts, and carbon credits. Gold tokenization is the most liquid commodity RWA market.

Why DeFi protocols want RWAs

The demand for RWAs inside DeFi is not purely ideological — it is financial. Stablecoin protocols, lending markets, and DAOs have accumulated enormous idle treasuries earning zero yield in crypto-native assets. As US interest rates climbed above 5%, tokenized T-bills became the obvious solution: real yield backed by sovereign debt, available 24/7, settleable in minutes rather than days.

MakerDAO (now Sky) was among the first large DAOs to move. It allocated over $1 billion of DAI backing into US Treasuries and corporate bonds via third-party RWA arrangers. The strategy earned the protocol hundreds of millions of dollars in annual revenue. Aave and Compound followed suit by proposing treasury diversification into tokenized money-market funds.

Permissioned tokens and why most RWAs are not freely tradable

Unlike ERC-20 memecoins that anyone can hold, most RWA tokens are permissioned. The issuer enforces KYC checks at the contract level — only wallets on the approved whitelist can receive transfers. This is required by securities law in most jurisdictions and by anti-money-laundering rules.

Permissioning limits composability. A whitelisted BUIDL token cannot be deposited into an anonymous DeFi lending pool. Some projects use wrapper tokens or intermediary stablecoins (like USDY as a yield-bearing stablecoin) to bridge between permissioned RWA exposure and DeFi composability, but these wrappers introduce additional counterparty risk.

Settlement finality and the T+0 promise

Traditional securities settle on a T+1 or T+2 cycle — you buy today, shares arrive in two business days. Tokenized assets settle in seconds to minutes, at any hour, any day of the week. This is the most concrete operational improvement tokenization delivers. For institutional prime brokers and cross-border capital flows, near-instant settlement has real cost implications: less collateral locked in settlement pipelines, less counterparty risk during the settlement window.

The tokenized Treasury market demonstrated this concretely when BUIDL processed over $1 billion in subscriptions and redemptions without a single T+1 settlement delay.

Risks unique to RWA tokens

- Custody risk: If the entity holding the underlying asset fails or misappropriates funds, token holders have legal claims but may face lengthy bankruptcy proceedings. The token contract cannot force an insolvent custodian to release assets.

- Oracle/attestation risk: If the off-chain attestation of asset value is delayed, manipulated, or simply stops, the token's claimed backing becomes unverifiable. Stale NAV data can mask losses.

- Regulatory risk: Securities laws vary by country. A token that is legal to hold in one jurisdiction may be classified as an unregistered security in another. Issuers may restrict redemption for wallets in certain regions with no advance notice.

- Liquidity risk: Secondary market liquidity for most RWA tokens is thin. Redemption goes through the issuer on business days, not a 24/7 DEX. In a risk-off environment, redemption queues can form.

- Smart contract risk: The token contract itself can have vulnerabilities. Distribution logic, whitelist management, and redemption flows are all attack surfaces.

How to evaluate an RWA product before investing

Before allocating capital to any tokenized asset, verify these five things:

- Who is the custodian, and are they regulated in a major jurisdiction? (Coinbase Custody, BNY Mellon, State Street are positive signals.)

- Is there a regular third-party audit or attestation of the underlying holdings, and is it publicly accessible?

- What is the legal structure — SPV, trust, or fund — and does it clearly entitle token holders to the underlying asset in insolvency?

- Are transfer restrictions enforced onchain (whitelist) and are you eligible to hold and redeem?

- What are the redemption terms — daily, weekly, T+2 — and is there a redemption gate or minimum hold period?

The regulatory outlook for RWA tokenization in 2026

Regulation of tokenized securities is maturing rapidly. The EU's DLT Pilot Regime created a sandbox for blockchain-based securities settlement. Singapore's MAS Project Guardian tested tokenized bonds and fund distributions with major banks. In the US, SEC guidance on digital asset securities has clarified that most tokenized equities and debt instruments fall under existing securities law — no special crypto exemption.

The practical effect is that institutional-grade RWA issuers are now operating openly under existing regulatory frameworks. This is good for investor protection but creates compliance overhead that keeps the market concentrated among well-capitalised issuers.

Where to follow the RWA market in real time

The RWA market moves fast. Track total on-chain RWA value at rwa.xyz. Monitor individual protocol developments through governance forums. For token-specific price and market data, see Ondo Finance and Centrifuge on our market pages. For a deep-dive on lending-focused RWA products, our Maple Finance review covers the platform in detail.

Summary: the realistic picture of RWA tokenization

Tokenizing real-world assets is not about putting physical assets on a blockchain — it is about replacing legacy settlement, custody, and transfer-agent infrastructure with programmable token contracts while maintaining traditional legal and custodial protections for the underlying asset. The technology delivers real benefits: faster settlement, 24/7 availability, programmable compliance, and composability with DeFi. The risks are real too: custody and legal risk are not eliminated, only repackaged. Investors need to evaluate the full four-layer stack, not just the token contract.

This article is for educational purposes only and does not constitute financial or legal advice. RWA products may be subject to securities law in your jurisdiction. Always conduct your own research.