Why real estate tokenization is harder than tokenizing bonds

Tokenized Treasuries and on-chain credit have grown rapidly because they tokenize liquid, fungible, standardized financial instruments with clear valuation and established legal custody infrastructure. Real estate is the opposite: illiquid, heterogeneous, jurisdiction-dependent, and requiring complex title, zoning, and maintenance infrastructure that a blockchain cannot replicate.

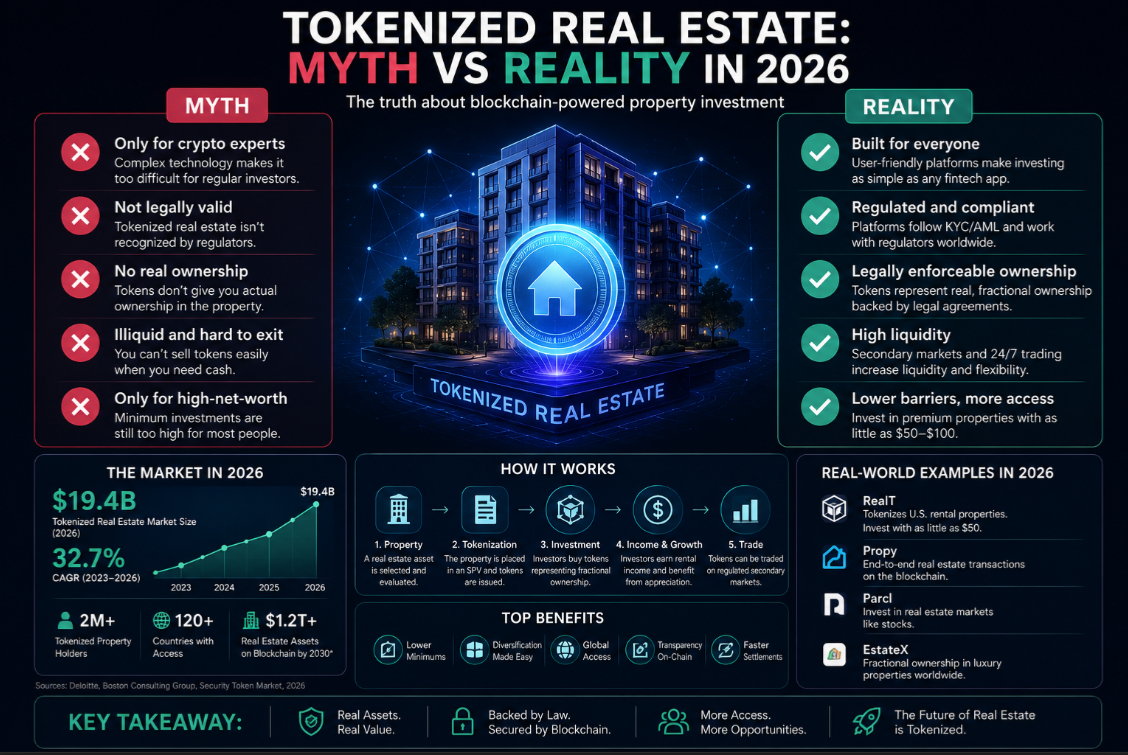

The promise of real estate tokenization is compelling: fractional ownership of high-value properties, global investor access, secondary-market liquidity, and automated yield distribution. The reality in 2026 is more modest — the market is real but small, regulatory fragmentation is severe, and most "liquid" tokenized real estate products are far less liquid than their marketing suggests.

How property tokenization actually works

The legal structure for tokenized real estate typically involves one of three models:

- SPV equity tokenization: A special-purpose vehicle (SPV, usually an LLC) holds title to the property. Investors purchase tokenized equity shares of the SPV. Ownership of the token equates to a fractional equity interest in the SPV, which in turn owns the property. This is the most common structure for single-property tokens.

- REIT tokenization: A regulated Real Estate Investment Trust issues tokenized shares or units. This brings REIT tax treatment and regulatory oversight but requires compliance with REIT rules (distribution requirements, asset tests). Franklin Templeton and Blackstone have explored tokenized REIT share classes.

- Debt tokenization: Rather than equity, investors hold a tokenized mortgage note or real estate bridge loan. Returns come from interest payments rather than property appreciation and rental income. Lower upside, but senior in the capital stack — losses are absorbed by equity first.

The liquidity problem: myth vs reality

The most frequently overstated claim in real estate tokenization is liquidity. Traditional real estate is deeply illiquid — selling a property takes weeks to months. Token proponents argue that a secondary market for tokens provides continuous liquidity. In practice:

- Thin secondary markets: Most tokenized real estate tokens trade on small alternative trading systems (ATS) or platform-specific marketplaces with minimal volume. Bid-ask spreads can be 5–10% and large sell orders move the market significantly.

- Jurisdictional transfer restrictions: Many property token transfers are subject to the same restrictions as traditional real estate sales — pre-emptive rights, lender consent, transfer tax. These cannot be automated away by a smart contract.

- NAV disconnects: Token prices on secondary markets can diverge significantly from underlying property NAV, especially during broad market downturns. A property worth $10M may have tokens trading at a 20% discount if sentiment sours.

- Redemption windows: Most tokenized real estate funds offer quarterly or annual redemption windows, not daily liquidity. Emergency sales require finding a buyer, not a DEX pool.

Leading tokenized real estate platforms in 2026

Several platforms have built working tokenized real estate products with real properties and real investor returns:

- RealT: US-based platform offering tokenized fractional ownership of US residential rental properties. Investors receive weekly rental income in USDC. Properties are held in individual LLCs. Token trading on RealToken Marketplace. Over 500 properties tokenized.

- Lofty.ai: Similar to RealT, focuses on US residential rental properties. Tokens available for as little as $50 per token. Income distributed daily on Algorand.

- Propbase: Southeast Asia-focused tokenized real estate, operating in Thailand and the Philippines. Uses Aptos blockchain.

- Landshare: Tokenized US real estate on BNB Chain with DeFi yield layer — LP farming on token pairs.

- Brickken: European platform offering tokenized real estate and other asset classes. Operates under EU crowdfunding and securities regulations.

Regulatory landscape: why it varies so dramatically by country

Real estate law is local. Property rights, transfer taxes, land registry rules, foreign ownership restrictions, and securities regulations differ radically between countries. A tokenized property structure that is legally clear in Delaware may be unenforceable in Singapore, require a licensed broker in Germany, or be outright prohibited for foreign investors in Thailand.

This creates two problems. First, most platforms operate in a single jurisdiction (usually the US or one EU country) and cannot offer global access. Second, the KYC/AML requirements for securities-law-compliant property token offerings create significant overhead that reduces the economic benefit of small fractional investments.

The most legally robust jurisdictions for tokenized real estate in 2026 are: the United States (via SPV equity or Reg D/S offerings), Liechtenstein (under the Blockchain Act), and the UAE (under ADGM and DIFC financial free zone rules). Singapore's MAS has also provided regulatory clarity under its Securities and Futures Act.

Yield and returns: what tokenized real estate actually delivers

US residential rental properties (RealT, Lofty) typically deliver 5–9% annual yield from rental income after platform fees and property management costs. Commercial properties can deliver higher yields (8–12%) but with higher vacancy risk and management complexity.

Importantly, tokenized real estate investors generally receive rental yield only — not property appreciation in liquid form. If the property value doubles, tokens may appreciate on secondary markets, but converting that appreciation to cash requires finding a buyer for your tokens or waiting for a sale/redemption event. This is structurally different from REITs, where NAV appreciation is reflected in a liquid publicly-traded share price.

The three biggest risks in tokenized real estate

- Platform risk: Most tokenized real estate platforms are young startups. If the platform fails, the property management infrastructure, income distribution, and secondary market disappear. Investors hold tokens in an SPV with no operational support. This risk is partially mitigated by the SPV structure (platform failure doesn't mean property loss) but practically devastating for income and liquidity.

- Vacancy and management risk: Rental income depends on tenants paying rent and the property being well-managed. Remote ownership with no local control means investors are fully dependent on the platform's property managers. Bad management, vacancy, or unexpected repair costs directly reduce yield.

- Legal enforceability risk: In a dispute, does holding a token genuinely entitle you to SPV equity and thus property income? The answer depends on jurisdiction-specific laws around electronic securities and LLC membership. Most structures have been designed by lawyers to be enforceable, but the legal precedents are thin in most countries.

When tokenized real estate makes sense

Tokenized real estate is most compelling in two specific scenarios. First, for investors in countries with restricted access to US or European real estate, tokenization removes the traditional barrier of requiring a local bank account, credit history, or large minimum investment. A $50 investment in a US rental property via a mobile app is genuinely novel access.

Second, for yield diversification: rental income from real property has low correlation to crypto market volatility. Adding 5–10% annual yield from real-world rents can stabilise a crypto-heavy portfolio. But the illiquidity of tokenized real estate means this allocation should be treated as a long-term position, not tactical.

Comparing tokenized real estate to REITs

- REITs: Publicly traded, high liquidity, professional management, diversified portfolio, regulated, tax-advantaged in many jurisdictions. Minimum investment: one share (~$10–$100 for ETF exposure).

- Tokenized real estate: Direct fractional ownership, on-chain yield distribution, global accessibility, but thin secondary markets, platform risk, and jurisdictional complexity.

For most individual investors, a diversified REIT ETF (VNQ, REET) delivers superior risk-adjusted real estate exposure compared to tokenized single properties. Tokenized real estate makes more sense for DeFi-native users who want on-chain yield and have specific geographic or property-type preferences that REITs don't serve.

What to look for before investing in a tokenized property

- Verify the legal structure: does holding the token clearly entitle you to SPV equity or fund units under the law of the relevant jurisdiction?

- Who holds property title and in what legal vehicle? Is the SPV bankruptcy-remote?

- What is the platform's track record? How many properties, what vacancy rates, how long have distributions been paid?

- Is there a secondary market, and what is the realistic bid-ask spread?

- What are the redemption options and timelines? Monthly, quarterly, or sale-only?

- What is the full fee structure (platform fee, property management fee, transaction fee)?

Summary: the honest state of tokenized real estate in 2026

Tokenized real estate is real, functional, and growing — but the liquidity and accessibility promises are partially overstated. The technology works for distributing rental yield on-chain and fractionalising ownership, but it does not solve the fundamental illiquidity of real property. Regulatory fragmentation limits geographic scope. Platform risk is significant for early-stage providers. The best use cases are access expansion (global investors reaching otherwise unavailable markets) and on-chain yield diversification for DeFi-native portfolios with long time horizons.

This article is for educational purposes only. Real estate investments involve risk of loss. Tokenized property products may not be available in your jurisdiction or may be restricted to accredited investors.