The case for tokenized equities

Public equity markets are among the most liquid in the world — but only if you live in the right country, have a brokerage account, and operate during market hours. For the two billion people globally without easy access to US or European stock markets, tokenized equities offer a new path: fractional ownership of Apple, Tesla, or an S&P 500 ETF, settled in minutes on a blockchain, accessible 24/7.

Beyond access, tokenized stocks promise programmable corporate actions (dividends auto-distributed as stablecoins), composability with DeFi (using tokenized TSLA as collateral for a USDC loan), and global portability (transfer shares cross-border without clearing houses). As of 2026, these promises are partially delivered — the market is growing but still nascent, with meaningful regulatory complexity and liquidity constraints.

How tokenized stocks are structured

There are two primary structural models for tokenized equities:

- Custodian-backed tokens: A regulated issuer purchases the actual underlying share and holds it with a licensed custodian (broker-dealer or custodian bank). They then issue a token on a blockchain representing a claim on that held share. This is the model used by Backed Finance and Ondo's Ondo Global Markets product. The token is legally a receipt for a held share, not the share itself.

- Synthetic tokens: The token tracks the price of a stock via a synthetic mechanism (collateral pool + price oracle) rather than holding actual shares. Higher capital efficiency, zero custody fees, but the token holder has no legal claim on the underlying company's equity — only a contractual right against the issuer.

Custodian-backed tokens are legally more robust; synthetic tokens are more capital-efficient and easier to construct for illiquid or hard-to-access equities. Most serious tokenized stock products in 2026 use the custodian-backed model.

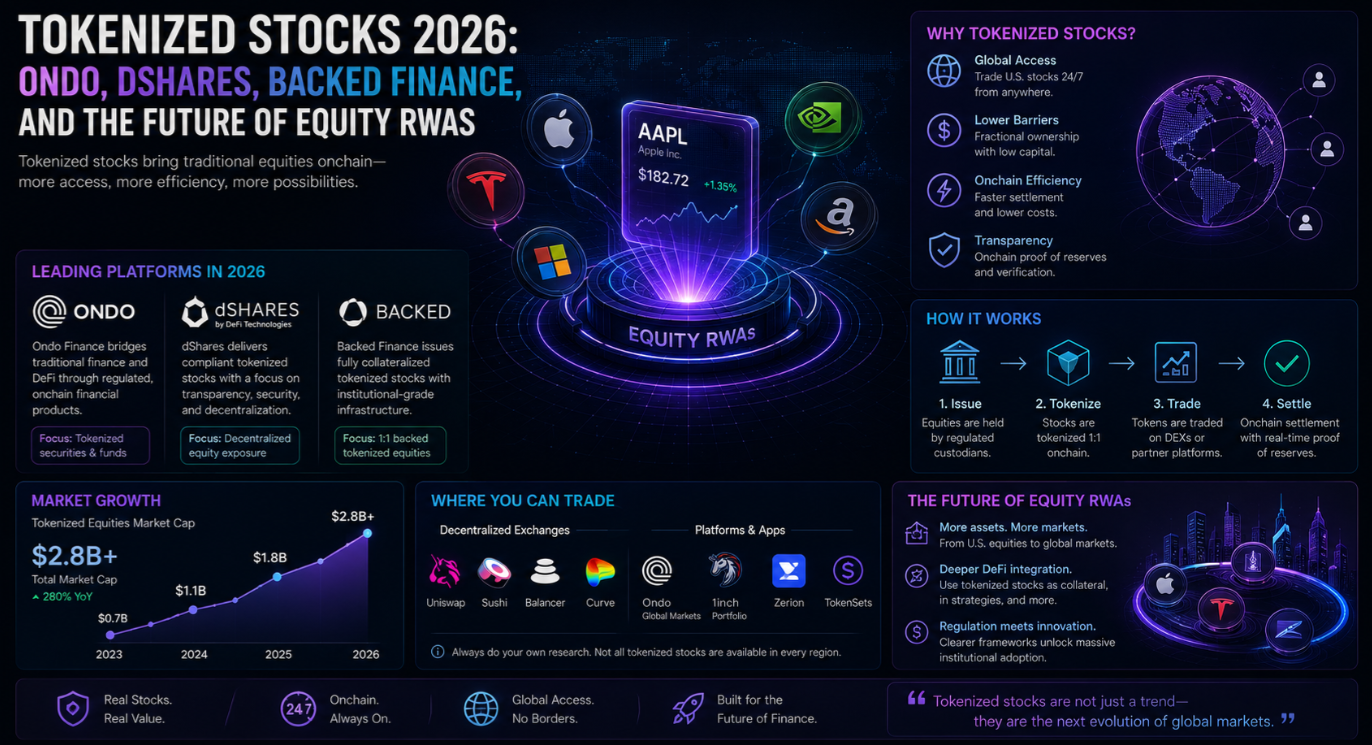

Ondo Finance and Ondo Global Markets

Ondo Finance is the most prominent tokenized securities issuer in the DeFi space. After establishing itself in the tokenized Treasury market with OUSG and USDY, Ondo launched Ondo Global Markets — a platform for tokenized US stocks and ETFs. It allows non-US qualified investors to purchase tokenized representations of major US equities and ETFs, with settlement in stablecoins and cross-chain support.

Ondo's model targets international investors who want US equity exposure without opening a US brokerage account. The ONDO governance token gives holders voting rights over protocol parameters and fee distribution. For ONDO price data and forecasts, see our Ondo Finance market page and Ondo Finance price forecast.

- Products: Tokenized US equities, ETFs, and T-bills (OUSG, USDY) under a unified compliance layer.

- Chains: Ethereum, Polygon, Mantle, Solana.

- Target users: Non-US qualified investors and institutions; DeFi protocols seeking composable RWA exposure.

- Compliance: On-chain KYC via Ondo's compliance layer; transfer restrictions enforced in the token contract.

Backed Finance: tokenized ETFs on Ethereum

Backed Finance issues tokenized representations of major ETFs and equities on Ethereum. Products include bCSPX (Coinbase-tracked S&P 500 ETF), bIB01 (iShares short-term Treasury ETF), bNVDA (NVIDIA stock), and bCOIN (Coinbase equity).

Backed's product is notably DeFi-composable: bIB01 has been integrated into Morpho Blue as lending collateral. The token uses a standard ERC-20 interface with transfer restrictions for KYC compliance. Backed operates under a Swiss financial intermediary framework and restricts US person access due to securities law.

- Key products: bCSPX, bIB01, bNVDA, bCOIN — custodian-backed ETF and equity tokens.

- Chain: Ethereum mainnet.

- DeFi use: Morpho Blue collateral, Spark Protocol integration.

- Restriction: Not available to US persons; targets European and Asian accredited investors.

dShares by Dinari: SEC-compliant tokenized US equities

Dinari's dShares are tokenized US equities designed to be compliant with US securities law from the ground up. Dinari operates as a regulated transfer agent — a licensed securities intermediary. Holders of dShares are actually registered on Dinari's transfer agent records as beneficial owners of the underlying shares, giving them stronger legal standing than a token receipt.

Dinari's regulatory approach makes dShares potentially available to US retail investors — a market that most tokenized stock products actively exclude. However, being subject to standard securities regulations also means trading hours align with US market hours and full KYC/AML is mandatory.

- Products: Tokenized shares of US-listed equities: AAPL, TSLA, NVDA, MSFT, and dozens more.

- Legal structure: Dinari as registered transfer agent; holders are beneficial owners on record.

- Chains: Ethereum, Arbitrum, Base.

- US person access: Available to US persons — a major differentiator from Backed and other competitors.

Mirror Protocol and its collapse: a cautionary tale

Any discussion of tokenized stocks must acknowledge Mirror Protocol — Terra's synthetic stock platform that at its peak handled billions of dollars in synthetic mAssets tracking Apple, Google, and Tesla prices. Mirror used algorithmic synthetic token mechanics rather than actual share custody.

When Terra/Luna collapsed in May 2022, Mirror Protocol collapsed with it. The synthetic token backing evaporated instantly. Holders of mAAPL or mTSLA received nothing — there were no actual shares held in custody, only an algorithmic peg maintained by UST liquidity that disappeared overnight. Mirror's collapse illustrates the existential difference between custodian-backed tokens and synthetic ones: when the underlying is actual equity held by a custodian, the token has real residual value even in a crisis.

Corporate actions: dividends, splits, and voting rights

One of the technically interesting aspects of tokenized stocks is handling corporate actions on-chain:

- Dividends: Cash dividends can be automatically distributed to token holders as stablecoins via smart contract, eliminating the multi-day dividend processing cycle of traditional brokers.

- Stock splits: A 2-for-1 split doubles the token supply to existing holders — straightforward to implement on-chain.

- Voting rights: Most tokenized stock products do NOT pass through voting rights to token holders in 2026. The custodian holds the share and votes it. Passing through governance to thousands of anonymous token holders is a solved technical problem but an unsolved legal and regulatory one.

- Proxy voting: Some platforms are exploring proxy voting through verified token holder identity, but this is not yet broadly available.

Regulatory status: the SEC, MiFID II, and the global patchwork

Tokenized equities face the most complex regulatory environment of any RWA category because they touch multiple regulatory domains simultaneously: securities law, market infrastructure regulation, broker-dealer licensing, and custodian regulation.

In the US, the SEC has signalled that tokenized securities must comply with existing securities law. This means issuers need to be registered broker-dealers or partner with them, operate registered transfer agent functions, and comply with Regulation ATS for secondary trading. The regulatory clarity is actually higher than in 2022 — the rules exist, issuers just need to follow them. Dinari's dShares approach is the most compliant US model.

In the EU, MiFID II financial instrument rules apply. Switzerland and Liechtenstein have enacted specific digital securities frameworks that provide cleaner legal paths. Singapore's MAS has active sandbox programmes. The common thread is that tokenized stocks are not a regulatory grey area — they are securities, and securities law applies.

Composability with DeFi: the holy grail

The most transformative use case for tokenized stocks is DeFi composability: using Apple or NVIDIA tokens as collateral to borrow stablecoins on Aave, or providing liquidity in TSLA/USDC pools. This is the vision that would genuinely disrupt traditional prime brokerage.

In 2026, partial composability exists. Backed's bIB01 is live in Morpho Blue. Some tokenized ETFs are used as DAO treasury collateral. Full DeFi composability for tokenized individual stocks remains limited by KYC requirements, permissioned token transfers, and the regulatory complexity of allowing anonymous DeFi borrowing against securities-classified collateral.

The long-term vision: programmable capital markets

The deepest promise of tokenized stocks is not fractional ownership of AAPL — Robinhood already enables that. The real innovation is programmable corporate actions, instant cross-border settlement, composable use as DeFi collateral, and the eventual convergence of securities and DeFi into a single programmable capital markets infrastructure. This convergence is a decade away at minimum, but the infrastructure being built today — Ondo Finance, Dinari, Backed — is laying its foundations.

Summary: the state of tokenized stocks in 2026

Tokenized stocks are real, regulated, and growing — but not yet mainstream. Ondo Global Markets leads for non-US DeFi-native access to US equities. Backed Finance provides DeFi-composable ETF tokens for European and Asian investors. Dinari's dShares offer the most legally robust US-accessible product. Synthetic models like Mirror Protocol demonstrated the catastrophic downside of custodian-free synthetic stock tokens. The near-term opportunity is access expansion for non-US investors; the long-term vision is programmable capital markets infrastructure that converges DeFi and traditional finance.

Tokenized securities are regulated financial instruments. This article is educational only and does not constitute investment advice. Availability varies by jurisdiction. Always consult a qualified financial and legal adviser before investing.