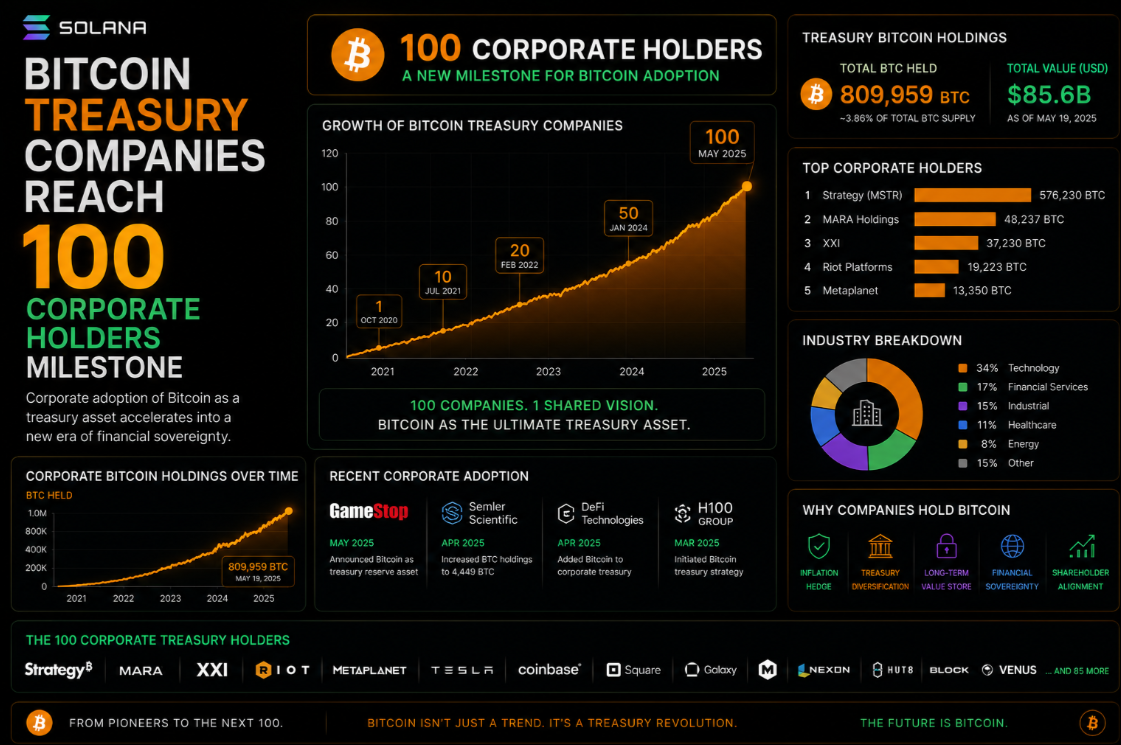

When MicroStrategy made its first Bitcoin purchase in August 2020, the move was widely mocked as a reckless gamble by a fading software firm. Five and a half years later, the same strategy has been replicated by more than 100 publicly listed corporations, marking a structural shift in how institutional finance views the world's largest cryptocurrency. The Bitcoin market page now reflects a demand floor underpinned by corporate balance sheets worth hundreds of billions of dollars.

How the 100-Company Milestone Was Reached

Reaching triple-digit corporate adopters required multiple catalysts to align. The approval of spot Bitcoin ETFs in the United States in January 2024 was perhaps the single most important trigger: it normalised Bitcoin as a mainstream asset class for institutional allocators and gave corporate finance teams the compliance cover they needed. Once major asset managers — BlackRock, Fidelity, Franklin Templeton — appeared in the same shareholder reports as Bitcoin-holding treasuries, the social stigma evaporated.

A second catalyst was the FASB's ASU 2023-08 accounting rule, which took effect for most public companies in early 2025. Under the old impairment-only model, a company that bought Bitcoin at $60,000 and watched it fall to $40,000 had to write down the loss — but could not write it back up when the price recovered. The new fair-value model treats Bitcoin like a marketable security, allowing both gains and losses to flow through the income statement. This symmetry removed a major objection from CFOs and audit committees.

The third driver was performance: companies that adopted Bitcoin treasury strategies outperformed their index peers significantly in 2024 and early 2025. That track record became a powerful recruiting tool for boards evaluating the strategy.

Breakdown of the 100 Corporate Holders

The 100 companies are not monolithic. They span at least a dozen sectors and four continents, though North America dominates. Technology firms represent the largest cohort, followed by financial services, mining, and energy companies. A smaller but growing group of traditional industrials — manufacturers, retailers, logistics firms — have also adopted Bitcoin as a secondary treasury asset.

Collectively, public companies hold roughly 700,000 BTC, representing about 3.3 % of the total 21 million supply cap. Adding private companies, exchange-traded products, and nation-state holdings, corporate and institutional entities now account for an estimated 12 % of all Bitcoin in circulation — up from under 2 % in 2020.

- Technology sector: ~38 companies, average holding 4,200 BTC

- Financial services: ~22 companies, average holding 8,100 BTC

- Bitcoin mining firms: ~18 companies, average holding 12,000 BTC

- Energy and resources: ~12 companies, average holding 2,900 BTC

- Other sectors: ~10 companies, average holding 1,400 BTC

The MicroStrategy Blueprint and Its Copycats

Strategy (formerly MicroStrategy) holds approximately 528,185 BTC as of Q1 2026, representing a cost basis near $35,000 per coin and an unrealised gain exceeding $12 billion. The company funds purchases through convertible notes and at-the-market equity offerings, essentially running a leveraged Bitcoin vehicle wrapped in a Nasdaq-listed shell. Its Bitcoin yield metric — percentage change in BTC held per diluted share — has become a popular benchmark for evaluating competing treasury strategies.

Smaller companies have adapted the blueprint to their own capital structures. Some issue preferred shares with Bitcoin-denominated dividends; others pledge BTC as collateral for operational credit lines. The common thread is treating Bitcoin not as a speculative trade but as a long-duration savings vehicle denominated in a fixed-supply currency.

For deeper context on price dynamics behind these balance sheets, see the Bitcoin price forecast and consider that institutional demand now forms a structural bid at multi-year horizons.

Regulatory Tailwinds Across Jurisdictions

Regulatory clarity has been a prerequisite for most corporate treasurers. The US SEC's shift from adversarial enforcement to structured rulemaking under 2025 leadership gave legal teams the comfort they needed. The EU's MiCA framework, fully operational from late 2024, provided a similar compliance scaffold for European corporates. Japan's Financial Services Agency issued updated guidance allowing listed firms to hold Bitcoin without triggering investment company reclassification.

Several jurisdictions — notably El Salvador, the United Arab Emirates, and Singapore — now offer explicit tax treatment for corporate Bitcoin holdings that makes periodic rebalancing less punitive than in the US. This has led to a wave of treasury structures domiciled in friendly jurisdictions while maintaining primary stock exchange listings in New York or London.

Investors seeking to gain exposure through vetted platforms can compare custody and trading options at the top exchanges rating or review major custodians individually, including Coinbase review.

Risks and Criticisms

Not everyone celebrates the corporate treasury trend. Critics argue that concentrating large BTC positions in leveraged public vehicles creates systemic risk: forced selling during a credit event at one highly levered holder could cascade into broader market pressure. Strategy's convertible debt maturities, spread across 2027-2031, are frequently cited as a potential stress test.

Shareholder activists at several companies have challenged Bitcoin treasury policies as outside the core competency of management, a misuse of capital that should be returned to shareholders, or an inappropriate risk for employees with pension exposure to company stock. These challenges have occasionally succeeded — two mid-cap firms reversed Bitcoin treasury programs in 2025 following proxy votes — but the majority of boards have maintained their positions.

What the Milestone Means for Bitcoin's Long-Term Price Structure

The 100-company milestone matters beyond symbolism. Corporate treasuries create a category of holder that is structurally unlikely to sell: finance departments governed by board policy, audit requirements, and public disclosure obligations do not make reactive trades. This structural holding reduces the effective float of Bitcoin available for day-to-day trading, tightening supply and creating persistent upward pressure on price during demand surges.

Models that adjust the stock-to-flow ratio to account for institutional and corporate lockups suggest a materially tighter supply dynamic than raw issuance figures imply. If the trend continues to 500 companies — a plausible scenario given current trajectory — the supply impact could be profound, reinforcing Bitcoin's role as a macro reserve asset comparable to gold in institutional portfolios.