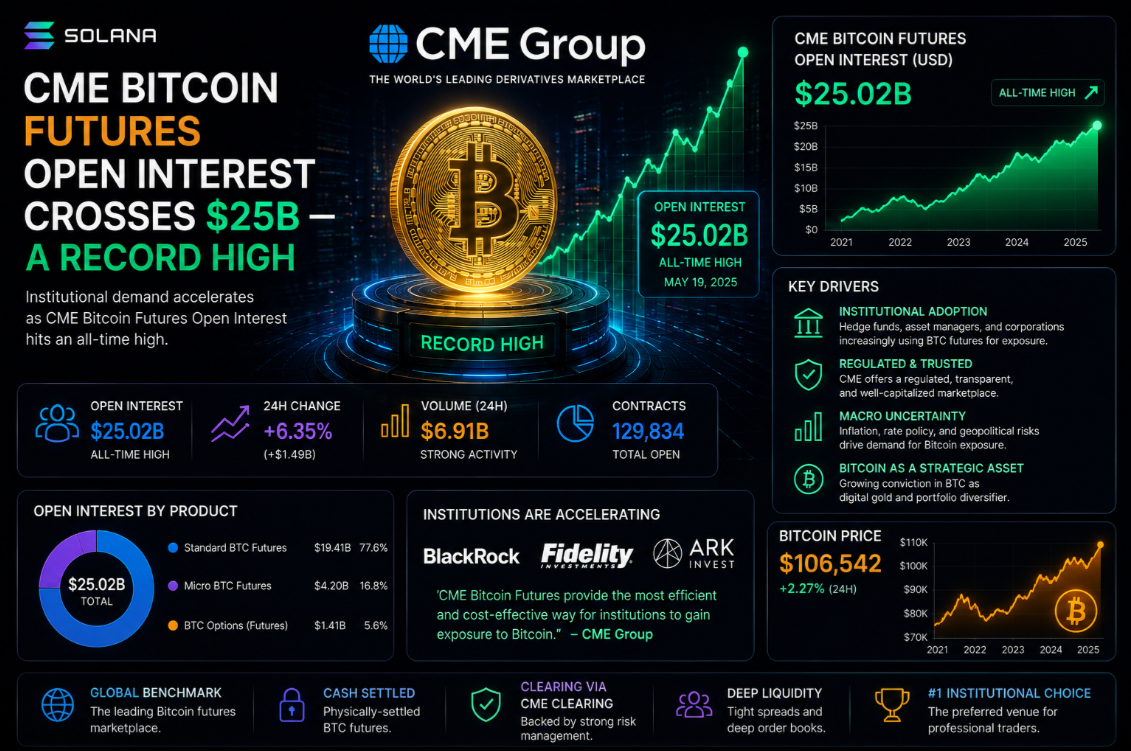

CME Group's Bitcoin futures market crossed a historic threshold in late March 2026 as open interest surpassed $25 billion for the first time in the exchange's history. The milestone confirms that Bitcoin has fully graduated into the institutional derivatives mainstream — a transition that began with the 2017 launch of the first CME Bitcoin futures contract but accelerated dramatically following the January 2024 spot ETF approvals. For context on how this demand is reflected in on-chain and spot markets, see the Bitcoin market data page.

From $1B to $25B: The CME Growth Trajectory

CME Bitcoin futures reached $1 billion in open interest for the first time during the bull market of late 2020. The journey from there to $25 billion was neither linear nor rapid: OI collapsed to below $500 million during the 2022 bear market, recovered to $10 billion in 2023, and then accelerated sharply post-ETF. The doubling from $12.5B to $25B required just eleven months — the fastest pace of growth the market has recorded.

Several structural factors explain the acceleration. First, ETF launch gave asset managers daily liquidity management tools: instead of buying and selling ETF shares, they use futures to adjust net exposure while keeping the ETF position intact for long-term allocation. Second, the options market on CME Bitcoin grew proportionally, attracting volatility arbitrage desks that must delta-hedge through futures. Third, macro funds began treating Bitcoin as a liquid risk-on proxy during policy uncertainty, adding and removing positions through CME rather than spot.

Who Is Holding These Positions?

CFTC Commitments of Traders (COT) reports provide a weekly snapshot of position holders. The most recent data shows:

- Asset managers (long-only funds, ETF managers): net long ~$9.2B notional

- Leveraged funds (hedge funds, CTAs): net long ~$4.8B, short ~$3.1B

- Dealers and intermediaries (market-making, basis trades): roughly neutral at scale

- Other reportables (family offices, endowments): net long ~$2.7B

- Non-reportable (smaller accounts): mixed, largely retail

Asset managers dominate the long side, consistent with passive accumulation tied to ETF inflows. Leveraged funds show more nuanced positioning: their gross short represents hedges and basis trades rather than outright bearish bets. The dealer community, roughly neutral overall, facilitates the enormous volume without taking directional risk.

The Basis Trade: Risk-Free Yield in a Bitcoin World

One of the most important developments embedded in the OI surge is the normalisation of the Bitcoin carry or basis trade. When CME front-month futures trade at an annualised premium of 10-15 % above spot, institutions can lock in that spread with near-zero directional risk: buy spot Bitcoin (or a spot ETF), short an equivalent notional in CME futures, and collect the premium at settlement.

For regulated institutions constrained from holding spot Bitcoin directly, the ETF-futures pair achieves the same economic result. At 12 % annualised, the basis trade offers returns competitive with investment-grade corporate bonds but with shorter duration and daily liquidity. This has attracted a category of fixed-income allocators who previously had no pathway into Bitcoin markets.

Traders evaluating exchange options for basis execution can review custody and fee structures at Binance review and explore broader rankings at top exchanges.

Volatility Implications of Record OI

Markets with large open interest in derivatives are not necessarily calmer — but they are better capitalised. CME margin requirements mean that every dollar of OI is backed by substantial collateral, reducing the risk of cascading liquidations that plagued unregulated offshore exchanges during 2022. Still, sharp macro surprises — Federal Reserve communications, geopolitical events, or regulatory announcements — can trigger simultaneous margin calls across many positions, amplifying short-term moves.

Key volatility risk periods tied to high CME OI include the days surrounding FOMC meetings, monthly futures settlement dates, and quarterly options expiries. Spot Bitcoin prices have historically shown elevated intraday swings of 3-5 % on these dates as positions are rolled or closed.

On a longer horizon, high institutional OI is generally associated with deeper liquidity and tighter bid-ask spreads in spot markets. More participants means more arbitrage activity keeping prices efficient across venues, which ultimately benefits all market participants from retail buyers to corporate treasury managers.

CME Micro Bitcoin and Options Market Depth

CME Micro Bitcoin futures (one-tenth of a BTC per contract) have grown in parallel with standard contracts, giving smaller institutions and proprietary traders precise position sizing without the minimum capital requirements of full contracts. Micro OI now represents roughly 8 % of total CME Bitcoin OI by notional value but a much higher share of contract count — reflecting democratisation of access to regulated Bitcoin derivatives.

The options market on CME has also expanded significantly. Put-call ratios, skew, and implied volatility surfaces are now tracked by institutional desks as leading indicators of sentiment. The existence of a deep options market enables hedging strategies that were previously impractical, further entrenching Bitcoin in institutional portfolios that require tail risk management.

What $25B OI Signals for Price Discovery

Price discovery in Bitcoin increasingly happens on CME during US trading hours, a reversal from the early years when offshore perpetual markets set the marginal price. Academic research using Hasbrouck information share methodology shows CME contributing 40-60 % of price discovery on high-OI days, up from under 15 % in 2021.

This shift has practical consequences: it means Bitcoin prices are more responsive to US macro data releases and Fed communications than to the retail sentiment indicators that dominated a few years ago. Traders who use on-chain metrics as timing tools must increasingly overlay CME positioning data to accurately forecast short-term price behaviour.

For long-run price projections that incorporate institutional demand factors, see the Bitcoin price forecast model.