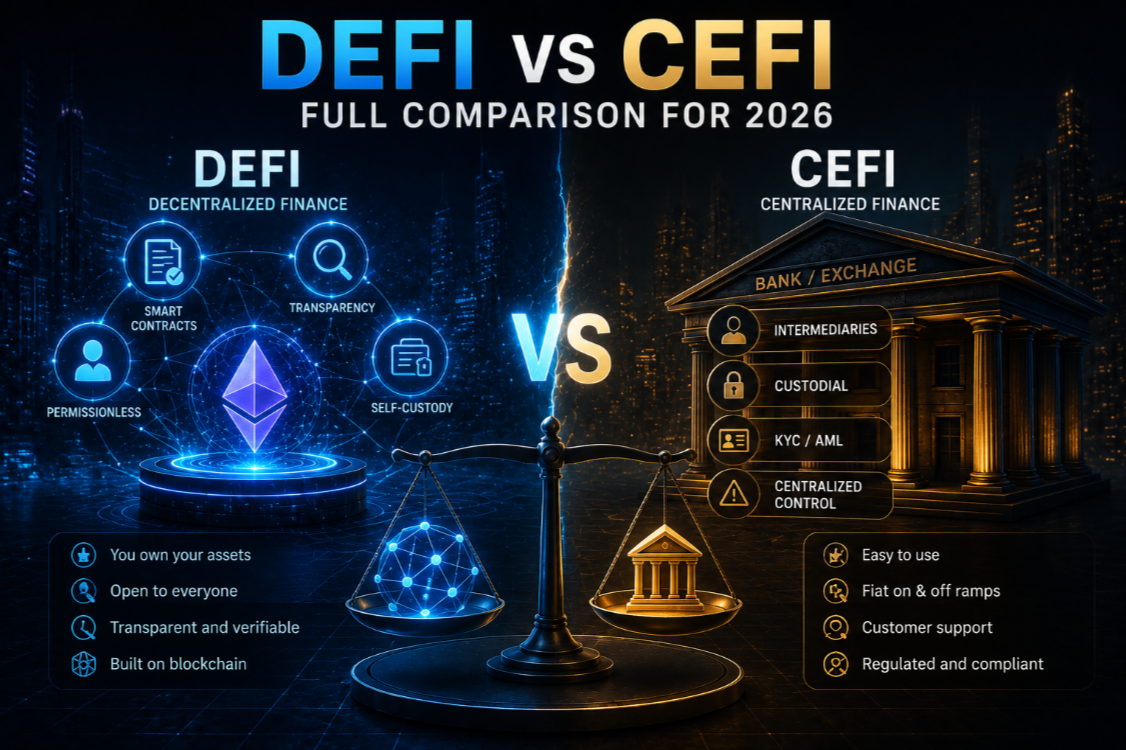

What is CeFi and why millions still use it

Centralised finance (CeFi) is the model most people know from traditional banking applied to crypto: a company holds your assets, handles custody, executes trades, and pays you yield. Coinbase, Binance, Kraken, and Nexo are CeFi platforms. You log in with a username and password, pass KYC, and trust the platform to keep your funds safe.

CeFi platforms excel at user experience. Fiat on-ramps, customer support, insurance on cash balances, and tax reporting tools make them the default entry point for most newcomers. The trade-off is counterparty risk: when FTX collapsed in November 2022, users lost billions because the exchange had custody of their funds. CeFi is convenient precisely because you hand over control.

What is DeFi and how it removes the middleman

Decentralised finance (DeFi) replaces intermediaries with self-executing smart contracts deployed on public blockchains like Ethereum. Nobody holds your funds except you — interactions are wallet-to-contract. Lending, borrowing, trading, and earning yield all happen on-chain, visible to anyone, auditable at any block.

The DeFi ecosystem in 2026 has over $120 billion in total value locked (TVL). Key protocols include Aave for lending and borrowing, Uniswap for decentralised token swaps, and Curve for stablecoin liquidity. Each runs without a corporate entity behind it — governed instead by token holders through on-chain voting.

Custody: self-sovereign vs trusting a company

The most fundamental difference between DeFi and CeFi is custody. In CeFi, the platform holds your private keys. In DeFi, you hold them. This single difference has enormous consequences.

- CeFi custody pros: Password recovery, customer support, no seed phrase to lose, regulated in most jurisdictions.

- CeFi custody cons: Platform bankruptcy, freezes, hacks, withdrawal gates, and geopolitical restrictions can block access to your funds at any time.

- DeFi self-custody pros: No counterparty risk, no KYC, censorship-resistant, works 24/7 without maintenance windows.

- DeFi self-custody cons: Full responsibility for seed phrase backup, no recovery if keys are lost, phishing and smart-contract risks fall entirely on the user.

The 2022–2023 wave of CeFi failures (Celsius, BlockFi, FTX, Voyager) shifted many experienced users toward DeFi self-custody. But for everyday users, CeFi still dominates on convenience.

Yield and interest rates: DeFi vs CeFi compared

Both DeFi and CeFi offer yield on idle crypto, but the mechanics and risk profiles are fundamentally different.

- CeFi yield: Platform-set rates, typically 2–8% APY on stablecoins. The yield comes from the platform's lending book. You don't see where your funds go. Rates have fallen sharply since 2022 as risk appetite dropped.

- DeFi yield: Market-driven rates updated block-by-block. On Aave, supplying USDC currently earns around 5–9% APY depending on utilisation. On Curve's 3pool, around 3–6% with additional CRV rewards. All cash flows are on-chain and auditable in real time.

- Liquidity mining bonuses: DeFi protocols often reward liquidity providers with governance tokens on top of base fees. This can inflate headline APYs dramatically, but token price risk makes these numbers unstable.

The DeFi yield is not free money — smart contract risk, liquidation risk, and impermanent loss are real costs not visible in the APY figure.

KYC and privacy: who knows your identity

CeFi platforms are regulated financial intermediaries in most jurisdictions. They are required to collect identity documents (KYC) and report transactions above certain thresholds to tax authorities. Your trading history, balances, and personal data are stored on their servers.

DeFi protocols interact with wallet addresses, not identities. There is no sign-up, no email, no passport scan. Transactions are pseudonymous — visible to anyone on-chain but not linked to a real-world identity unless you reveal it. Governments are increasingly pushing for DeFi KYC rules, and some front-ends (like Uniswap Labs' interface) already block sanctioned addresses via on-chain screening tools.

Smart contract risk: the DeFi-specific danger

DeFi's biggest unique risk is smart contract failure. A vulnerability in the protocol code can allow an attacker to drain all funds in seconds. Unlike a bank hack, there is no FDIC insurance, no customer support line, and usually no reversibility. Notable exploits in recent years include the Ronin bridge ($625m), Wormhole ($320m), and Euler Finance ($197m — though most funds were returned).

Mitigation steps: use only audited protocols with multi-audit histories and bug bounty programmes. The Aave review covers how Aave's security model and audit trail compares to competitors. Never put more into a single protocol than you can afford to lose entirely.

Regulatory risk: which is safer in 2026

CeFi faces direct regulatory pressure: licencing, capital requirements, travel rule compliance, and asset segregation mandates. This creates overhead but also legal protections for users in regulated jurisdictions.

DeFi protocols are decentralised by design, making them harder to shut down, but front-ends, developers, and large token holders have been targeted by enforcement actions (SEC vs Uniswap Labs, CFTC vs Ooki DAO). Regulatory risk in DeFi is more unpredictable — individual users may have less exposure but protocol availability could be restricted in certain regions.

Transaction speed and costs

CeFi trades settle internally in milliseconds at zero fee to the user (the exchange profits from the spread). Fiat withdrawals take hours to days depending on the bank.

DeFi transactions settle on-chain in seconds to minutes. Gas fees on Ethereum mainnet can range from under $0.10 on quiet days to $20+ during congestion. Layer 2 networks (Arbitrum, Optimism, Base) have brought fees to fractions of a cent, making DeFi practical for smaller amounts. Uniswap is fully deployed on L2s with sub-cent swap fees.

Composability: DeFi's killer advantage

DeFi protocols are composable — they plug together like Lego blocks. A single transaction can borrow from Aave, swap on Uniswap, deposit into Curve, and stake the LP token in a yield aggregator, all atomically. This programmable money stack has no CeFi equivalent. Flash loans — uncollateralised loans that must be repaid within one transaction — are a DeFi-only primitive used for arbitrage, liquidations, and complex strategies.

Who should use DeFi vs CeFi in 2026

- New to crypto, < $1,000: CeFi (Coinbase, Kraken) — easier onboarding, fiat rails, customer support.

- Intermediate, holding $1,000–$50,000: CeFi for fiat on/off ramp + DeFi for yield and active participation. Use hardware wallet.

- Advanced, > $50,000: Primary DeFi self-custody with hardware wallet + multisig, CeFi only for liquidity when needed.

- Privacy-conscious users: DeFi by default, with privacy-preserving tools and L2s to reduce on-chain footprint.

- DAOs and protocols: DeFi-native treasury management using Gnosis Safe + Aave + Curve. See our DeFi ratings.

The hybrid model: CeFi + DeFi in practice

Most experienced participants use both. A typical setup: buy crypto via CeFi for fiat access → withdraw to hardware wallet → interact with DeFi for yield → convert back to fiat via CeFi when needed. This captures the convenience of CeFi entry/exit while keeping the custody and yield advantages of DeFi in the middle.

Summary: DeFi vs CeFi at a glance

- Custody: DeFi (self) vs CeFi (platform)

- Yield: DeFi (market-driven, higher) vs CeFi (platform-set, lower)

- KYC: DeFi (none) vs CeFi (required)

- Smart contract risk: DeFi (yes) vs CeFi (no, but counterparty risk)

- Composability: DeFi (yes) vs CeFi (no)

- Fiat rails: CeFi (yes) vs DeFi (no native fiat)

- Customer support: CeFi (yes) vs DeFi (community forums only)

This article is for educational purposes only. Not financial advice. Crypto carries significant risk of loss. Always conduct your own research.