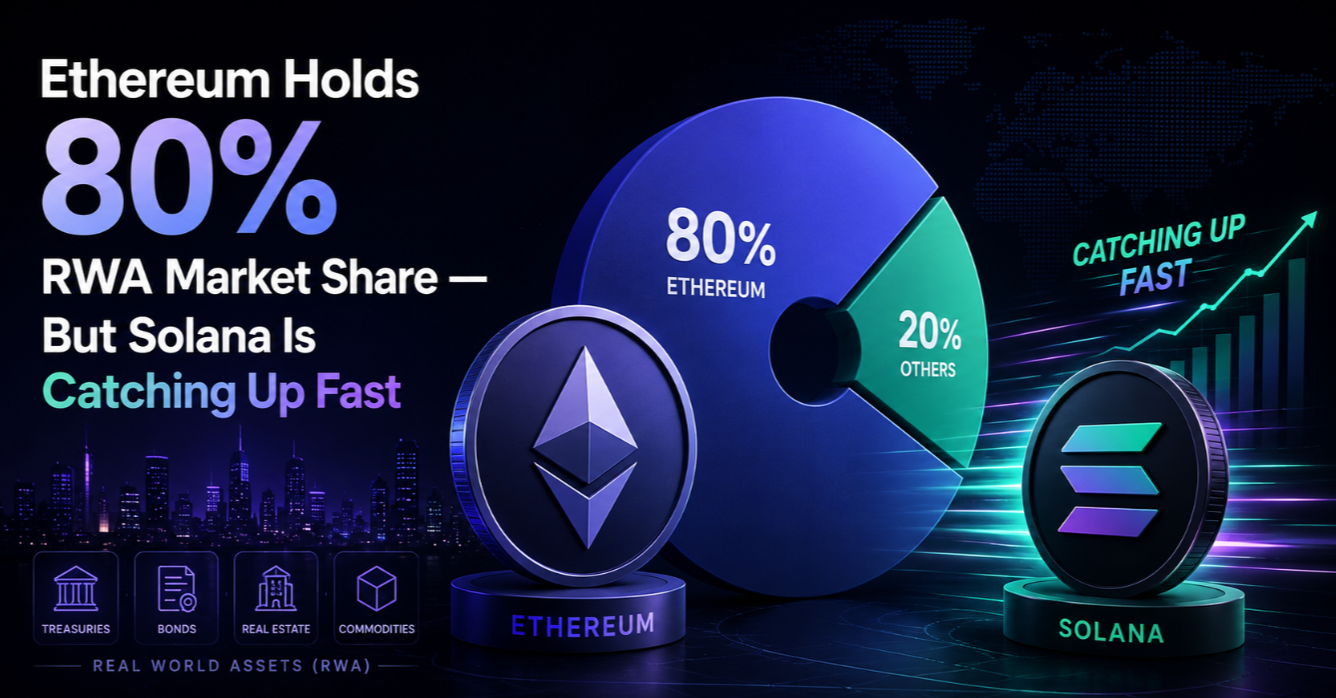

Ethereum's dominance of the real-world asset tokenization market remains overwhelming at roughly 80% of total on-chain RWA value — approximately $11.2 billion of the $14 billion total as of April 2026. But the trend line tells a more nuanced story: Solana's RWA share has tripled from under 2% to 6% in twelve months, and the deployment of BlackRock BUIDL on Solana signals institutional intent to accelerate that growth. The chain race for RWA dominance is the most consequential infrastructure competition in blockchain today. See Ondo Finance market data for live metrics on the leading cross-chain RWA protocol.

Ethereum's Structural Advantages in RWA

Ethereum's 80% market share was not achieved through marketing — it reflects genuine structural advantages that have compounded over years of institutional adoption. The ERC-1400 security token standard, developed specifically for compliant token issuance with transfer restrictions, was the de facto choice for the first wave of institutional tokenization projects beginning in 2022-2023. Legal teams at major asset managers had already reviewed ERC-1400 implementations, auditors had experience with the standard, and regulators had begun forming views on Ethereum-based securities.

The second structural advantage is the depth of the institutional smart contract audit ecosystem. Firms like OpenZeppelin, Trail of Bits, and Consensys Diligence have conducted thousands of Ethereum smart contract audits. When a compliance officer at a $500 billion asset manager asks "who has audited this token contract?", they want to see a name they recognise with a track record they can verify. Solana's audit ecosystem, while growing, has fewer credentialed firms and a shorter track record.

Third, Ethereum L2s have extended the base chain's reach without fragmenting compliance infrastructure. Polygon's institutional RWA suite, Arbitrum's growing DeFi ecosystem, and Avalanche Evergreen subnets all settle ultimately to Ethereum-compatible security models. Centrifuge is a prime example — its structured credit pools operate on Ethereum's EVM infrastructure and benefit from this institutional tooling depth.

Solana's Accelerating RWA Footprint

Solana's RWA growth from ~$280 million in April 2025 to ~$840 million in April 2026 — a 200% increase — was not organic DeFi activity. It was driven by specific institutional decisions, most notably BlackRock BUIDL's Solana deployment and Ondo Finance's cross-chain expansion of OUSG and xStocks products onto Solana.

The performance case for Solana in RWA is straightforward. Consider a tokenized money-market fund that distributes yield daily to 10,000 token holders. On Ethereum mainnet, 10,000 daily distribution transactions could cost $80,000-400,000 in gas annually — a meaningful drag on a product with a 4.5% yield. On Solana, the same 10,000 transactions cost less than $3. This is not a marginal difference; it changes the fundamental economics of small-account yield distribution.

- Ethereum RWA TVL (April 2026): ~$11.2B (80% share)

- Stellar RWA TVL: ~$560M (4% share — long-standing CBDC and remittance use cases)

- Polygon RWA TVL: ~$420M (3% share)

- Solana RWA TVL: ~$840M (6% share, up from 2% twelve months prior)

- Aptos/Sui combined: ~$140M (1% share, fastest growing percentage)

- Other chains: ~$840M (6% share)

The Compliance Infrastructure Gap

The most significant obstacle to Solana's RWA ambitions is not technical — it is compliance infrastructure. Institutional asset managers need on-chain KYC registries, whitelisted token transfer frameworks, programmable compliance rules, and audit trails that satisfy regulatory requirements across multiple jurisdictions. Ethereum has a three-year head start building this infrastructure.

Solana's compliance ecosystem has accelerated in 2025-2026. Securitize ported its compliance registry to Solana for the BUIDL deployment. Ondo built its own access control framework for xStocks and OUSG on Solana. Civic and Fractal ID provide on-chain identity verification on Solana. But these are project-specific solutions, not the standardised, audited, broadly-adopted frameworks that Ethereum has developed.

Maple Finance's institutional credit platform, reviewed in depth at Maple Finance review, operates primarily on Ethereum and Solana but has found compliance tooling on Solana requires more custom work than equivalent Ethereum deployments. This gap is narrowing but real.

Multi-Chain as the Endgame: Not Winner-Take-All

The framing of "Ethereum vs Solana" for RWA dominance may be misleading. The most likely long-term outcome is a multi-chain world where different asset types and use cases find their natural chain home:

- Large, infrequently-traded institutional assets (private credit, real estate, infrastructure): Ethereum mainnet or permissioned Ethereum subnets — security and compliance depth matter most

- High-frequency yield distribution and retail-facing products (money market funds, tokenized Treasuries): Solana or Ethereum L2s — fee minimisation and throughput matter most

- CBDC-adjacent and regulated financial institution use cases: Stellar, Corda, or custom blockchain infrastructure — direct institutional control and regulatory integration matter most

- DeFi composability and collateral use cases: wherever the deepest DeFi liquidity exists, currently Ethereum ecosystem

Protocols that abstract the multi-chain complexity for investors — like Ondo Finance, which deploys the same OUSG product across Ethereum, Solana, and Mantle — will likely capture more value than chain-maximalist approaches. For the most current view on how the market prices this multi-chain RWA thesis, see the Ondo Finance price forecast.

What the Chain Race Means for RWA Investors

For investors, the Ethereum vs Solana competition has a practical implication: the emergence of multi-chain RWA protocols means that chain selection is no longer an investor decision — it's an infrastructure decision made by the protocol. Ondo Finance holders benefit from OUSG being deployable on multiple chains; they don't need to manage cross-chain positions themselves.

The competition also drives fee reduction and performance improvement across both chains. Ethereum's L2 ecosystem will continue compressing transaction costs; Solana's Firedancer client upgrade in 2026 further improves its performance ceiling. Both dynamics benefit end users. The real-world asset tokenization market — projected to exceed $100 billion by 2030 — is large enough for multiple chains to prosper. The question is not which chain wins, but which protocols build the best multi-chain infrastructure on top of all of them. Centrifuge and Ondo are currently leading that race.