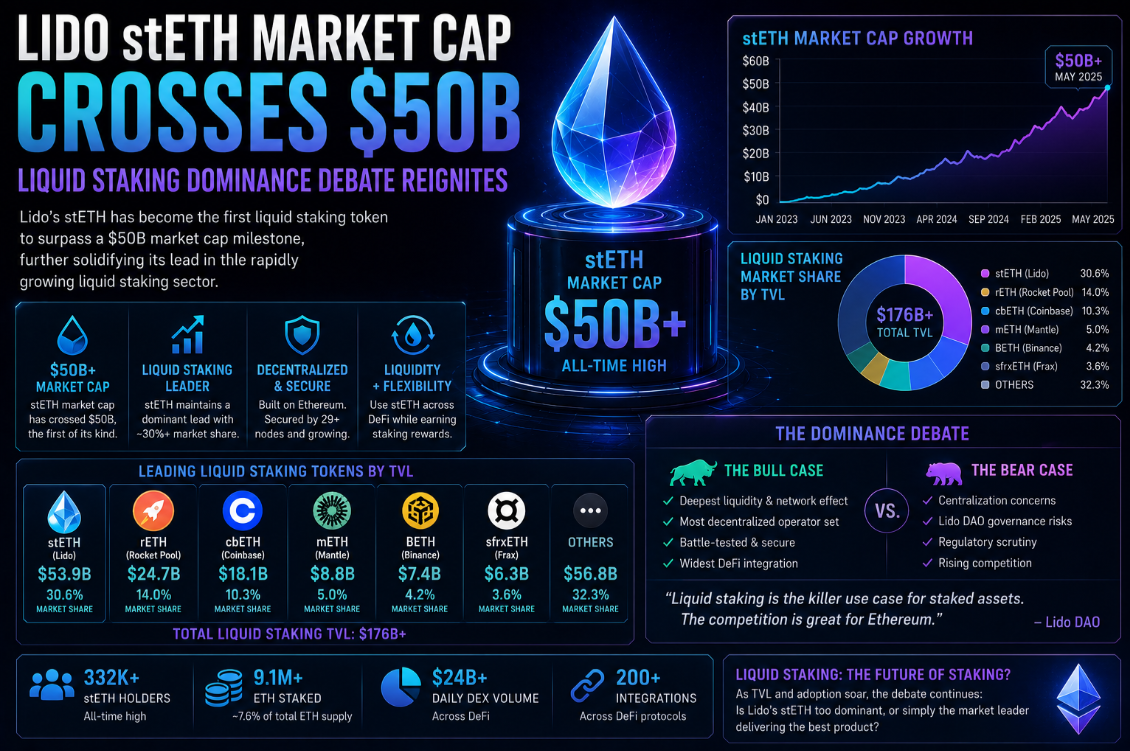

Lido Finance's stETH token crossed a $50 billion market cap in early April 2026, cementing its position as the dominant liquid staking derivative in DeFi and reigniting a long-running debate about protocol concentration on Ethereum. With more than 30% of all staked ETH flowing through a single protocol, Ethereum researchers, rival staking teams, and governance participants are wrestling with a question that has no clean answer: at what point does a successful protocol become a systemic risk to the network it secures? You can track real-time Lido metrics on the Lido DAO market page.

How stETH Reached $50 Billion

Lido launched in December 2020, less than two weeks after Ethereum's beacon chain went live, at a time when staked ETH was locked with no withdrawal mechanism. By solving the liquidity problem — giving stakers a tradeable receipt token — Lido captured early depositors who wanted yield without illiquidity. That first-mover advantage compounded: stETH's deep DeFi integrations on Curve, Aave, and MakerDAO made it the preferred ETH collateral, attracting more deposits, which deepened liquidity further.

The Shapella upgrade in April 2023 enabled ETH withdrawals, reducing Lido's structural liquidity advantage. Many analysts expected market share to erode as native staking became more accessible. Instead, stETH's share stabilised and then grew: DeFi composability proved stickier than the liquidity premium alone. Institutions and protocols that had already built stETH into treasury strategies, yield strategies, and collateral frameworks had no incentive to migrate.

By Q1 2026, approximately 12.4 million ETH was staked through Lido — out of roughly 41 million ETH staked in total. At a prevailing ETH price near $4,000, that translates to just over $49.6 billion, now past $50B. For detailed yield and operator data, the Lido full review covers risks, fee structure, and how stETH compares to alternatives.

The Dominance Debate: Arguments on Both Sides

Critics of Lido's scale are not fringe voices. Ethereum Foundation researchers including Justin Drake and Danny Ryan have publicly called for voluntary self-limitation, arguing that no single entity — even a DAO — should control more than 22% of staked ETH (the threshold below which a single attacker cannot cause delayed finality under current consensus parameters).

The case against Lido's dominance rests on three points. First, correlation risk: Lido's 30+ node operators are diverse but all subject to the same smart contract risk, the same DAO governance, and the same slashing parameters — a systemic bug or governance attack affects all of them simultaneously. Second, governance capture: the LDO token, which governs Lido, is concentrated among VCs and early investors who could theoretically override stETH holder interests. Third, regulatory surface: a single dominant protocol creates an obvious target for regulatory action in jurisdictions seeking to control Ethereum staking.

The case for Lido is equally substantive. The operator set is meaningfully decentralised — no single operator controls more than 5% of Lido's stake. Dual governance, introduced in 2025, gives stETH holders a direct veto mechanism against DAO decisions they consider hostile. Lido's market share growth reflects genuine user preference, not coercion; alternatives exist and are accessible.

Lido v3: Staking Vaults and Operator Diversity

The most significant technical development addressing centralisation concerns is Lido v3's staking vault architecture, released in beta in Q4 2025. Vaults allow institutional operators and DAOs to create customised staking pools that route through Lido's node operator network while maintaining independent risk parameters. A vault can specify operator whitelists, custom fee splits, and independent slashing insurance — effectively turning Lido into a modular staking middleware layer rather than a monolithic protocol.

Community operators — independent validators who meet Lido's technical and bond requirements — can now join the network through the Community Staking Module (CSM). CSM validators supply 2 ETH in bond per 32 ETH validator and are subject to the same performance monitoring as institutional operators. This opens Lido participation to a much wider pool of smaller operators, moving the protocol closer to Rocket Pool's permissionless model while preserving the liquidity depth that makes stETH useful.

stETH in DeFi: The Composability Moat

Understanding why stETH commands a premium requires understanding its DeFi footprint. stETH is accepted as collateral on Aave (where it underpins billions in borrowing), used in Curve's stETH/ETH pool (one of the deepest liquidity pools in DeFi), and integrated into dozens of yield strategies on Yearn, Convex, and Pendle. This composability creates a network effect: liquidity providers and DeFi protocols prefer the most liquid collateral, which is stETH, which attracts more liquidity, which deepens DeFi integrations further.

Pendle Finance's separation of stETH yield into principal tokens (PT-stETH) and yield tokens (YT-stETH) added a new dimension: traders can now take leveraged views on Ethereum staking yield without taking on ETH price risk. PT-stETH has become a popular fixed-income substitute for DeFi-native treasuries, further embedding stETH into institutional DeFi workflows.

- Aave v3: stETH collateral enabling ~$4.2B in ETH borrowing

- Curve stETH/ETH pool: ~$1.1B liquidity, <0.1% price deviation from ETH

- Pendle PT-stETH: ~$800M in fixed-yield positions

- MakerDAO/Sky: stETH accepted as collateral for DAI minting

- EigenLayer: stETH restakeable via liquid restaking protocols

Competitive Landscape and the Path Forward

Lido's dominance faces pressure from multiple angles. EigenLayer's restaking ecosystem has created new yield opportunities that favour protocols like EigenLayer and its liquid restaking wrappers (eETH, rsETH, pzETH) over plain stETH. Rocket Pool continues to grow methodically, particularly among users who prioritise decentralisation. Frax Ether and StakeWise v3 offer alternative models with different risk profiles.

The next major decision facing the Lido DAO is whether to implement voluntary market share limits — a proposal that has been debated but never adopted. With stETH at $50B and community pressure mounting, 2026 may force a definitive answer. The outcome will shape not only Lido's trajectory but the entire liquid staking landscape and Ethereum's security model for the next decade. Compare top staking platforms at the staking ratings page.