What is restaking?

Restaking is the practice of taking already-staked ETH — or a liquid staking token that represents staked ETH — and opting it into securing additional decentralized services beyond the Ethereum base layer. In plain terms: you use one pool of cryptoeconomic security to back multiple networks simultaneously, without needing to lock up additional capital for each one.

Traditional proof-of-stake staking is single-purpose. When you stake ETH, that ETH secures the Ethereum consensus layer and earns consensus-layer rewards. Restaking extends the security surface of that same ETH to external protocols — oracle networks, data availability layers, cross-chain bridges, rollup sequencers, and other middleware services — each of which pays its own rewards in return for the coverage.

The concept was pioneered by EigenLayer, which launched on Ethereum mainnet in 2023 and grew to over $20 billion in total value locked by 2025. Competing restaking layers have since appeared on other chains. For current market data on the EigenLayer token, see the EigenLayer market page, and for a full platform assessment see the EigenLayer review.

How EigenLayer works

EigenLayer sits as a smart contract layer on top of Ethereum. To restake, you deposit ETH or a liquid staking token (stETH, rETH, cbETH) into EigenLayer's restaking contracts. This action extends your existing staking commitment: your capital is now bound not just by Ethereum's slashing conditions but by any additional conditions imposed by the external services you choose to secure.

The architecture has three layers of participants. First, Restakers — individual holders who deposit ETH or LSTs and delegate to Operators. Second, Operators — professional node runners who register with EigenLayer and commit to running the software stack for one or more AVS. Third, AVS (Actively Validated Services) — the external protocols that consume the pooled security and distribute rewards back to operators and restakers.

When you restake, you choose an Operator and delegate your capital to them. The Operator's on-chain stake is the cryptoeconomic guarantee that the external service can rely on — if the Operator cheats or violates an AVS's rules, their stake (including your delegated capital) can be slashed. EigenLayer calls this "programmable slashing": each AVS defines its own slashing conditions through smart contracts that EigenLayer enforces.

- Step 1: Deposit ETH or LST (stETH, rETH, cbETH) into EigenLayer contracts

- Step 2: Delegate deposited stake to a registered Operator

- Step 3: Operator opts into one or more AVS and runs their node software

- Step 4: AVS distributes rewards to Operator; Operator shares a portion with restakers

- Step 5: Slashing conditions fire on-chain if Operator violates AVS rules

EigenLayer does not create new security from nothing — it redistributes Ethereum's existing cryptoeconomic security to services that would otherwise need to bootstrap their own validator sets from scratch. The trade-off is concentrated risk: a failure in one AVS can propagate losses to all restakers delegated to that Operator.

Actively Validated Services (AVS): what they are and why they matter

An Actively Validated Service is any decentralized protocol that requires a set of nodes to perform off-chain computation, attest to data, or enforce rules — and wants to borrow Ethereum's cryptoeconomic security to back those nodes rather than creating a new token and validator set from scratch. The AVS developer writes EigenLayer-compatible contracts that define reward distribution and slashing conditions, then advertises to Operators.

In 2025–2026 the live AVS ecosystem spans several categories:

- Data availability layers — Services like EigenDA provide off-chain data availability for rollups. Rollup operators post transaction data to EigenDA nodes (who are EigenLayer Operators) instead of posting everything to Ethereum calldata, drastically reducing rollup costs.

- Oracle networks — Decentralized price feeds and off-chain data providers that use restaked ETH as their security bond instead of native oracle tokens.

- Cross-chain bridges — Bridge validator sets secured by restaked ETH rather than their own staking token, reducing the cost and risk of bridging assets between chains.

- Rollup sequencers — Decentralized sequencer sets for Layer 2 rollups that require liveness and ordering guarantees backed by restaked capital.

- Coprocessors — Off-chain compute networks (ZK proof generation, verifiable AI inference) that post results on-chain and need a slashable stake as an honesty guarantee.

Each AVS sets its own reward rate, slashing conditions, and Operator requirements. Some AVS have deployed with live mainnet slashing enabled from day one; others started with "no-slashing" testnet phases before activating full conditions. As a restaker, it is essential to understand which AVS your chosen Operator services and whether those AVS have live slashing — because that determines your actual risk exposure beyond standard Ethereum consensus slashing.

Liquid restaking tokens: eETH, ezETH, rsETH

Liquid restaking protocols wrap the entire EigenLayer restaking position into a single tradeable token — the liquid restaking token (LRT). Just as Lido issues stETH for staked ETH, liquid restaking platforms issue their own receipt tokens that represent staked ETH + EigenLayer delegation + accumulated rewards from both layers. The holder of an LRT earns the combined yield without needing to interact with EigenLayer directly.

The three dominant LRT protocols in 2026 are ether.fi (eETH), Renzo (ezETH), and Kelp DAO (rsETH). Each routes user deposits into EigenLayer, selects and manages Operator delegation, and issues a liquid token that appreciates as rewards accumulate. The protocols charge a management fee (typically 5–15% of rewards) and handle the complexity of Operator selection, AVS monitoring, and rebalancing.

- eETH (ether.fi) — Ether.fi is the largest liquid restaking protocol by TVL. It issues eETH (rebasing) and weETH (wrapped, non-rebasing) and additionally distributes ether.fi points redeemable for ETHFI governance token rewards. Ether.fi operates its own Operators, giving it more control over AVS selection and slashing risk management.

- ezETH (Renzo) — Renzo abstracts Operator and AVS selection completely, automatically diversifying restaked ETH across multiple Operators and AVS to optimize yield and reduce concentration risk. Issues ezETH as its liquid token and distributes ezPoints for RENZO governance token.

- rsETH (Kelp DAO) — Kelp DAO launched as a multi-LST liquid restaking platform accepting stETH, ETHx, and sfrxETH as deposits. rsETH accrues both base LST yield and EigenLayer AVS rewards. Kelp distributes KELPMiles for KelpDAO governance token rewards.

LRTs are composable DeFi assets: eETH and ezETH are accepted as collateral on Aave, Compound, and various lending protocols, allowing holders to borrow against their restaking position or loop leverage. This composability significantly multiplies potential yield — and potential liquidation risk if the LRT depegs relative to ETH.

Restaking risks: slashing cascade and systemic fragility

Restaking stacks multiple layers of risk on top of each other. Understanding each layer is non-negotiable before committing capital. The risks are not merely additive — they can compound in ways that are difficult to model in advance.

- Consensus-layer slashing — Base Ethereum validator slashing applies to any natively restaked ETH. If the underlying Operator double-signs on Ethereum consensus, a portion of staked ETH is burned and the validator is ejected. This risk exists whether or not EigenLayer is involved.

- AVS slashing — On top of consensus-layer risk, each AVS with live slashing conditions adds an additional slashing surface. If an Operator misbehaves according to an AVS's rules — e.g., signing conflicting data in an oracle AVS — the AVS smart contract can slash a portion of the Operator's EigenLayer-registered stake.

- Slashing cascade — Because a single Operator can service multiple AVS simultaneously, a slashing event on one AVS can compound with others. If an Operator's stake falls below a threshold due to a first slashing event, it may trigger liquidations or reward disruptions across all AVS they service — even ones where they did not misbehave.

- Operator concentration risk — EigenLayer's Operator set is currently concentrated. The top 10 Operators control the majority of delegated TVL. If a single large Operator is slashed or exits, the impact on restaker capital and on AVS security is disproportionate.

- LRT smart contract risk — Liquid restaking protocols (ether.fi, Renzo, Kelp) add additional smart contract layers. A bug in an LRT contract, an EigenLayer contract, or an AVS contract could lead to total loss of funds in a worst-case exploit.

- LRT depeg risk — Like stETH during the 2023 banking stress event, LRTs can trade at a discount to their underlying ETH value during market dislocations. If you need to exit quickly, you may have to sell at a discount rather than waiting for the full redemption process.

- Rehypothecation risk — Using an LRT as DeFi collateral to borrow more ETH, then restaking the borrowed ETH, creates a leverage loop. A slashing event or LRT depeg at any point in the loop can trigger cascading liquidations across lending protocols.

EigenLayer explicitly warns in its documentation that restaking is an advanced DeFi operation not suitable for all users. The additional yield comes from additional risk — it is not free money. Start with a small allocation, use only a single AVS operator, and avoid LRT leverage loops until you have a deep understanding of each layer.

Yield breakdown: native staking, restaking, and points

The full restaking yield stack in 2026 has three components that combine to produce a total advertised APY that can appear much higher than simple ETH staking. Understanding each component separately is critical for evaluating actual risk-adjusted returns.

- Layer 1 — Ethereum consensus yield (3.5%–5% APY): The base layer. Every validator securing the Ethereum beacon chain earns consensus rewards proportional to their effective balance. This yield is paid in ETH and is the most reliable component — it changes slowly based on the number of active validators.

- Layer 2 — AVS rewards (0.5%–7% APY, variable): Each AVS distributes its own reward token to Operators and restakers. Reward rates vary enormously by AVS, fluctuate with AVS activity levels, and are often paid in the AVS's native governance token rather than ETH. Token rewards are subject to price volatility and vesting schedules — an AVS paying 8% APY in its own token at current prices could be worth much less if the token price declines.

- Layer 3 — Loyalty points (variable, non-guaranteed): Most major LRT platforms distribute platform-specific points (ether.fi points, ezPoints, KELPMiles) to depositors. These points are later converted to governance tokens during token generation events (TGE). The implied APY from points depends entirely on the token's launch price — points are not financial instruments with a guaranteed value.

A realistic 2026 yield estimate for a restaker using a liquid restaking protocol: 3.5%–5% ETH base yield + 1%–4% AVS rewards (denominated partly in governance tokens) + variable points. The honest cash-equivalent APY, stripping out governance token appreciation assumptions, is typically 4%–7% — roughly double native staking yield, in exchange for meaningfully higher complexity and risk.

Top liquid restaking platforms compared

For a full scored comparison of liquid restaking platforms on security, yield, smart contract audits, and UX, see the Staking platform ratings. The table below summarizes the key parameters for the three leading LRT protocols as of 2026.

- ether.fi — TVL: $8B+. LRT: eETH / weETH. Operator model: proprietary operators. Additional rewards: ETHFI token. Audits: 5+ independent audits (Sigma Prime, Cantina, others). Fee: ~10% of rewards. Unique: native ETH restaking (deposits ETH directly, no intermediate LST).

- Renzo — TVL: $3B+. LRT: ezETH. Operator model: multi-operator diversification. Additional rewards: RENZO token. Audits: 3+ (Halborn, Certik). Fee: ~10% of rewards. Unique: automatic AVS diversification, multi-LST deposits accepted.

- Kelp DAO — TVL: $2B+. LRT: rsETH. Operator model: curated multi-operator. Additional rewards: KelpDAO token. Audits: Sigma Prime, Code4rena. Fee: ~10% of rewards. Unique: accepts stETH, ETHx, sfrxETH directly; broad LST compatibility.

All three platforms integrate with EigenLayer as the underlying restaking infrastructure. Depositing into any of them counts toward EigenLayer's total restaked TVL. For DeFi yield strategies that layer on top of LRT positions, see the guide to best DeFi yield strategies 2026.

Restaking on Solana and Symbiotic: beyond Ethereum

EigenLayer is Ethereum-native, but the restaking primitive has been adopted across other ecosystems. On Ethereum itself, Symbiotic launched in 2024 as a competing restaking protocol with a more modular design — it accepts a wider range of collateral assets (not just ETH and LSTs) and allows AVS to define their own collateral policies. Symbiotic attracted significant backing and TVL within its first year, and by 2026 operates alongside EigenLayer as a second major restaking layer for Ethereum-based protocols.

On Solana, native restaking does not yet exist in the same form as EigenLayer — Solana's single-slot finality and different validator economics make direct analogues complex to implement. However, Solana's liquid staking ecosystem (Jito, Marinade) provides a foundation for restaking-like products. Several teams are building Solana-native shared security layers, and Jito's stake-weighted quality of service mechanism already functions as a primitive form of restaking: JitoSOL holders implicitly back the Jito block engine's operation and receive MEV rewards as their compensation.

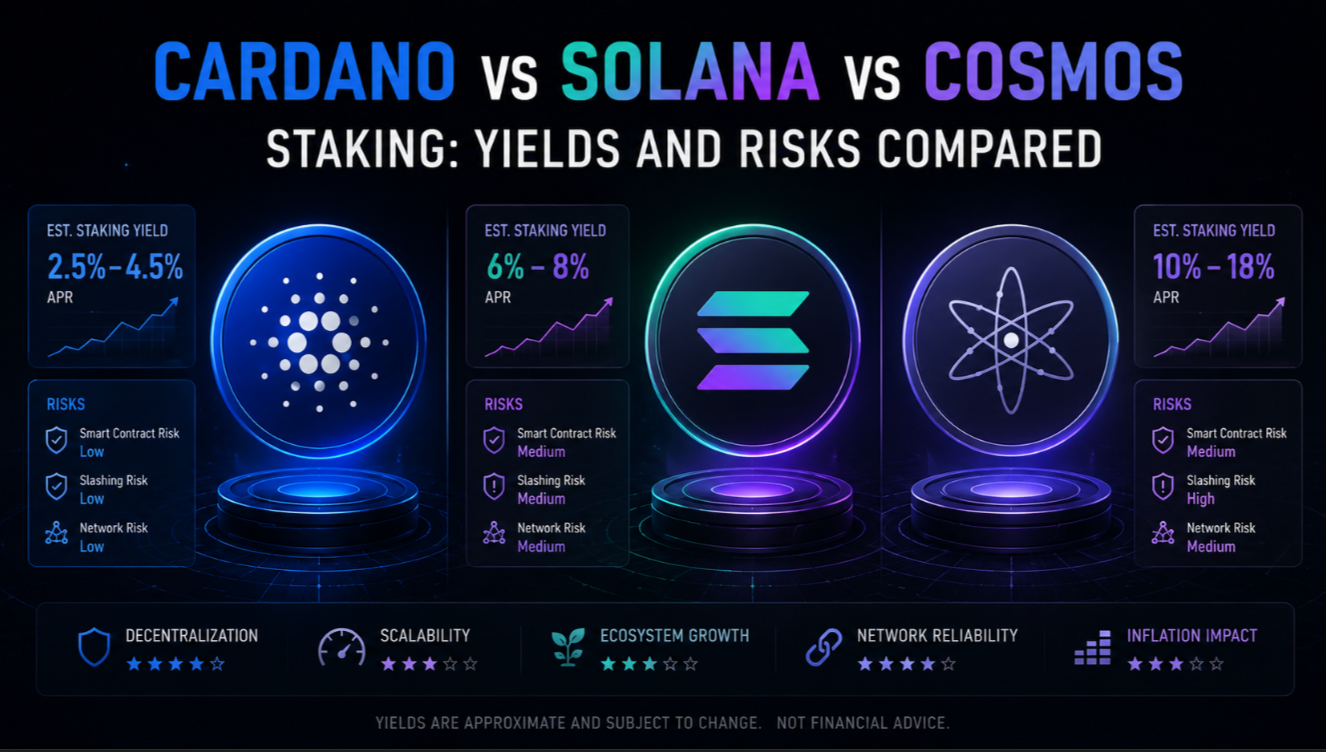

Cosmos and Polkadot have had shared security models from earlier in their development — Cosmos via Interchain Security (ICS) and Polkadot via its parachain slot auction model. These are architectural predecessors to restaking: a hub chain's validator set secures consumer chains, with the hub's stakers bearing both the risk and rewards of covering multiple chains. EigenLayer's innovation was packaging this concept for Ethereum's permissionless, smart-contract environment.

For most retail users in 2026, Ethereum-based restaking via EigenLayer (directly or through an LRT protocol) is the only mature, liquid, and widely supported restaking option. Solana and cross-chain restaking products are earlier-stage and carry additional smart contract and ecosystem risk.

Tax implications of restaking

Restaking introduces tax complexity beyond standard staking because it layers multiple income streams — each with potentially different timing and character — and involves several token conversion events. The following is general information; consult a qualified crypto tax professional for advice specific to your jurisdiction.

- Base staking rewards — ETH staking rewards are taxable income at fair market value when received in most jurisdictions (US, UK, Germany, Australia). The same applies to rewards received via a liquid staking token like stETH: either as daily rebases (stETH) or as accumulated exchange rate appreciation (rETH/weETH), depending on local treatment.

- AVS token rewards — Rewards received in AVS governance tokens are taxable income at the token's fair market value on the date of receipt. If the governance token has no established market price at launch (many AVS tokens launch with limited liquidity), valuation can be complex — some tax authorities accept a cost basis of $0 for tokens with no determinable value at receipt.

- LRT conversions — Depositing ETH into an LRT protocol and receiving eETH or ezETH may be treated as a taxable swap (ETH → eETH) in some jurisdictions. Redemption (eETH → ETH) is similarly a disposal event. Wrapping or unwrapping (eETH ↔ weETH) may also trigger recognition depending on local treatment.

- Points and TGE events — Points themselves are not taxable until converted to tokens at a TGE. The TGE conversion is typically a taxable receipt of income at the token's fair market value on TGE date. This can create a large tax liability in the TGE year even if you do not sell the tokens.

- Slashing losses — A slashing event that destroys part of your staked capital is typically treated as a capital loss at the value destroyed on the date of slashing. Maintain transaction records of any slashing events.

Use dedicated crypto tax software (Koinly, TaxBit, Cointracker, or Rotki for self-hosted) that supports EigenLayer and LRT protocol integrations. Manual tracking of daily stETH rebases, AVS reward claims, and LRT exchange rate changes across multiple positions is error-prone and impractical at scale.

How to start restaking: a step-by-step guide

Restaking is not for absolute beginners. Before attempting any of the steps below, you should already be comfortable with self-custody wallets, have experience with liquid staking (stETH, rETH), and understand the slashing risks described in section 5 above. If you are new to staking entirely, start with the guide to

best staking platforms 2026 first, and only return to restaking after you have run a liquid staking position for at least one month.

- Get ETH and set up a self-custody wallet. You need ETH in a wallet you control — MetaMask, Rabby, or a hardware wallet (Ledger/Trezor) connected to a browser wallet. Do not attempt restaking via a CEX — you need direct contract access. Use the Ethereum market page to monitor price and network conditions.

- Stake ETH via Lido to get stETH (optional but common). Many LRT protocols accept ETH directly, but if you already hold stETH from an existing Lido position, you can deposit it directly into EigenLayer or an LRT. Review the Lido review to understand Lido's current risk profile before adding an EigenLayer layer on top.

- Choose a path: direct EigenLayer or liquid restaking protocol. Direct EigenLayer: go to app.eigenlayer.xyz, deposit ETH or LST, choose an Operator with a verified track record and limited AVS exposure. This path gives you direct control but no liquidity — your position is not tokenized. Liquid restaking: go to ether.fi, Renzo, or Kelp, deposit ETH or LST, receive an LRT. This path gives you a liquid token usable in DeFi but adds an extra smart contract layer.

- Research the Operator (for direct EigenLayer). Review the Operator's on-chain history, the specific AVS they service, whether those AVS have live mainnet slashing, and the Operator's total delegated TVL. Prefer Operators with: (a) long operational history, (b) diversified AVS coverage without concentration in high-risk early-stage AVS, (c) public identity and transparent communication.

- Start with a small allocation. Begin with an amount you are comfortable losing entirely to a worst-case slashing or smart contract exploit. Restaking is higher risk than base staking — treat your first restaking position as an education cost, not a yield optimization from day one.

- Monitor slashing conditions and AVS status. Check the EigenLayer dashboard weekly. Monitor whether any AVS your Operator services have activated live slashing. Follow the Operator's communication channels (Discord, Twitter/X) for notices about AVS upgrades or incidents. Set up on-chain alerts via Tenderly or Forta for slashing events.

- Review platform ratings before scaling up. Before deploying significant capital, consult the EigenLayer review and the staking platform ratings for current security assessments.

Restaking in 2026 offers one of the highest legitimate yield opportunities in the Ethereum ecosystem — combining base staking yield, AVS rewards, and governance token incentives. The cost is meaningfully higher complexity and stacked slashing risk. The restakers who fare best are those who invest significant time in understanding each layer before deploying capital, who diversify across multiple Operators, and who treat governance token rewards as a speculative bonus rather than a core yield assumption.