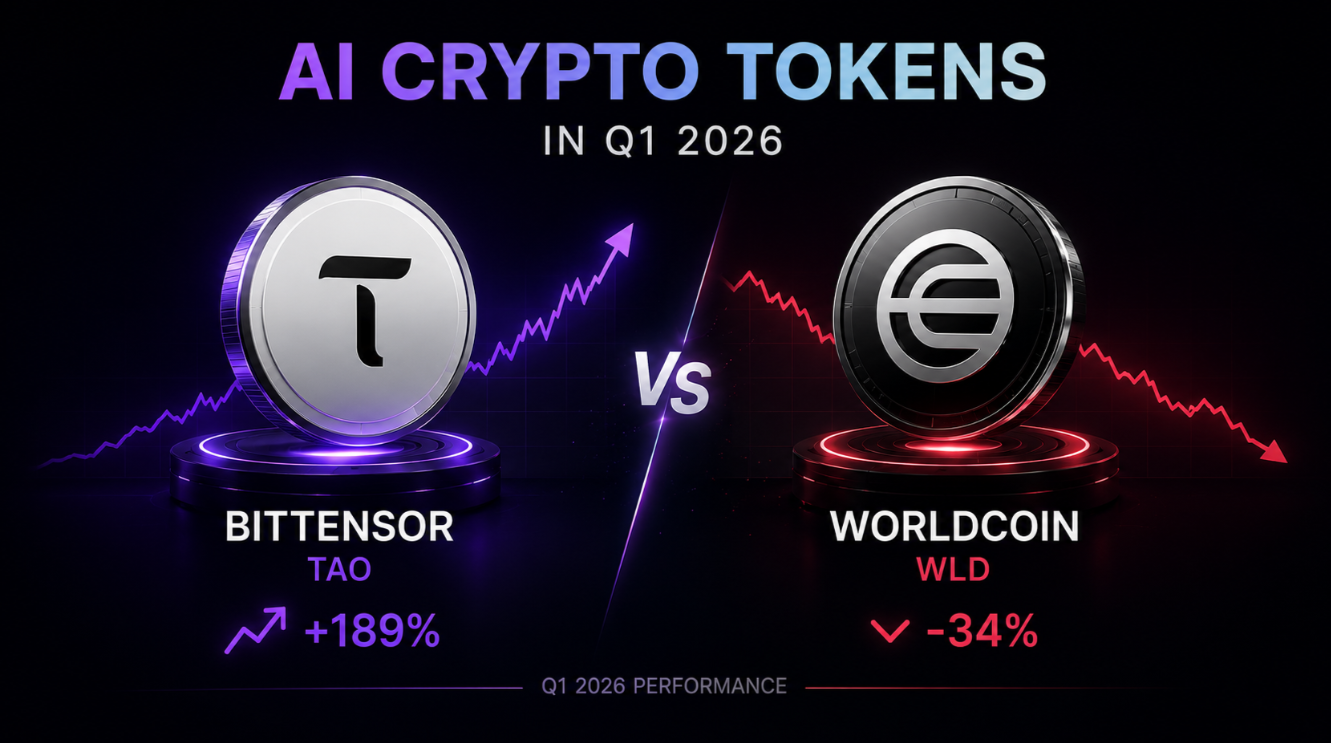

Q1 Winners: Bittensor Breaks $300 on Subnet Explosion

Bittensor (TAO) dominated the AI-token narrative in Q1 2026, climbing from a low of $187 in January to highs near $320 by late March. The catalyst was not new features but market repricing around the dTAO subnet-token explosion. When the dTAO upgrade shipped in February 2025, every subnet gained its own alpha token bonded against TAO through on-chain bonding curves. In Q1 2026, that mechanic finally drew sustained capital inflows. Traders and subnet developers rotated into 5–10 high-signal subnets, locking TAO into bonding curves and lifting the base asset price in the process.

Three milestones powered the rally: (1) SN1 Apex Chat subnet surpassed $50M in TVL, attracting serious model developers; (2) SN64 Chutes inference subnet released batch-processing APIs that LLM application teams could actually use without writing custom validators; and (3) Opentensor Foundation announced plans to bridge alpha tokens to Solana, lowering friction for retail buyers. The subnet market grew from ~80 active subnets in January to 127 by March. Most of the new entrants were low-TVL; a few were genuine experiments in on-chain RL agents and time-series prediction. The trend is clear: TAO is repricing on optionality, not today's usage.

For deeper analysis of Bittensor mechanics and valuation, see our Bittensor market page.

Q1 Losers: Worldcoin Halves Amid Regulatory Pushback

Worldcoin (WLD) painted the inverse picture. The project started 2026 near $6.50 and finished March around $3.20, a 51% drawdown. The root causes: (1) EU regulators raided Worldcoin Foundation offices in Madrid and Berlin in late February over data privacy claims; (2) Argentina revoked the project's biometric license, forcing shutter of operations; (3) India announced intent to ban the Orb network entirely; and (4) new TradFi research flagged that retention in the token-grant program has collapsed—far more new users are claiming free tokens and dumping than were expected based on 2022–2024 data.

Worldcoin's original narrative was simple: global identity + UBI via biometric Orbs + WLD token. The execution has been messy. The Orb expansion plan, which projected 500+ locations by Q1 2026, stalled at ~380 after regulatory headwinds in Europe and Asia. Each new rejection is a signal that the biometric-identity thesis has regulatory risk that the market had underpriced. WLD holders are now repricing the "network effect" scenario downward and asking harder questions about tokenomics (the foundation controls 45% of supply) and the long-term value of a token-claim program if regulatory restrictions force the project to retreat to a few friendly jurisdictions.

For broader context on Worldcoin's market position, visit the Worldcoin (WLD) market page.

The Middle Ground: Render, Fetch.AI, and NEAR Gain on Utility

Render (RNDR), Fetch.ai (FET, now rebranded ASI post-SingularityNET merger), and NEAR Protocol took a steadier path in Q1 2026. Rather than riding pure narrative momentum, these three benefited from concrete product milestones and adoption metrics.

Render climbed from $7.20 in January to $9.80 by March, driven by a combination of factors: (1) GPU supply constraints for AI inference continued to widen the margin for decentralized compute; (2) Anthropic and OpenAI both published research citing on-chain GPU markets as a risk vector, lending credibility to Render's pitch; (3) the Crescent decentralized rendering platform shipped a stable public API, allowing three indie game studios to deploy real workflows; and (4) RNDR staking fees hit an annualized 15%, attracting liquidity providers. Render is not explosive, but it captures the AI-compute cycle without the regulatory risk of identity projects.

Fetch.ai (now ASI) announced the completion of its merger with SingularityNET and Ocean Protocol in late Q1. The combined entity offers autonomous agents (Fetch infrastructure) + decentralized AI services (SingularityNET) + data trading (Ocean) under one token. The merger came with token conversion: 1 FET + 0.432 AGIX + 0.55 OCEAN → 1 ASI. Holders repriced on three counts: (1) the combined roadmap is clearer; (2) duplicate community overhead is gone; (3) but the token structure is now more complex for new entrants. ASI traded from ~$2.10 to ~$3.40 over Q1, a 62% gain, though much of it was front-running the merger announcement. The real test will be whether the unified entity executes on autonomous-agent adoption in the 2026 H2.

NEAR Protocol gained 18% over Q1 (from $5.10 to $6.02) on the back of a single product release: Chain Signatures, a native multi-chain signing primitive. The feature allows NEAR accounts to hold assets and sign transactions on Ethereum, Solana, Bitcoin, and other chains directly from a NEAR smart contract. This is differentiated infrastructure relative to cross-chain bridges; it removes the liquidity fragmentation problem that has plagued multi-chain apps. Three major DeFi protocols announced plans to port their NEAR deployments to multi-chain via Chain Signatures by end of Q2 2026. NEAR is gaining adoption because it solves a real engineering problem, not because of AI hype—but the narrative overlap with "AI agents that transact" is real, and traders are pricing that in.

For detailed market analysis on Render, visit the Render (RNDR) market page. For Fetch.ai and ASI details, see Fetch.ai market page. For NEAR Chain Signatures and adoption, see NEAR Protocol market page.

The Throughline: On-Chain Inference vs. Infrastructure

A second-order narrative has emerged from Q1 volatility: the market is splitting into two camps over what "AI crypto" actually means. Camp 1 (Bittensor, Worldcoin, some Fetch.ai discourse) wants on-chain inference—models running natively on decentralized networks, validators scoring outputs. Camp 2 (Render, NEAR, Eigenlayer restakers) wants AI infrastructure—GPU markets, signing primitives, data markets, agent tooling—without necessarily running inference on-chain.

The distinction matters. On-chain inference is capital-efficient (one model per subnet, many validators) but latency-heavy and economically harder to justify for real-time tasks. Infrastructure plays are capital-intensive (lots of GPUs, bandwidth) but economically simpler: pay for compute, get a result, move on. Q1 results suggest the infrastructure narrative is winning with developers. Render signed meaningful studio partnerships; NEAR attracted multi-chain deployments. Bittensor is winning on speculation, not developer traction—the dTAO upgrade and subnet bonding curves are powerful optionality tools, but they do not ship a working model-serving market yet.

In the long run, the winner is probably not binary. AI inference on decentralized networks will find a niche in privacy-critical and censorship-resistant use cases. Infrastructure tokens will capture the bulk of capital deployed to actual compute and serving. Q1 2026 is early; the market is still sorting which is which.

Regulatory Shadows and Headwinds Ahead

A theme that cut across the Q1 AI-token landscape was regulatory scrutiny. Worldcoin faced raids and operational shutdowns. The SEC stepped up enforcement activity around staking-yield claims on tokens like TAO, NEAR, and RNDR, with warning letters to two major exchanges offering yield products. The EU published draft guidance on "algorithmic governance" that directly called out protocol tokens and validator rewards as potential securities.

For projects like Bittensor and Fetch.ai, the risk is that validators, subnet owners, and token holders could be treated as participants in a "collective investment scheme" rather than as utility users. The defense is simple: the token is not necessary to receive the service (miners on Bittensor do not need to hold TAO). But the regulatory posture is hardening. Projects that can cleanly separate token economics from service access are de-risking faster than those that cannot.

Looking Ahead to Q2 and Beyond

As Q2 2026 begins, the AI-crypto sector is at an inflection. Bittensor has momentum but unproven subnet economics. Worldcoin is in crisis-management mode. Render, Fetch.ai, and NEAR are building quietly with real developer adoption. The sector has learned from past hype cycles: flashy tokenomics and narrative alone are not enough. Projects need defensible infrastructure, regulatory clarity, and actual users. Q1 was a reminder that volatility is here to stay, but so is capital. The question is whether AI-token projects can redirect hype into construction.

This page is information, not financial advice. Past performance does not predict future results. Do your own research before investing.